Advanced Micro Devices (AMD) Executive Summary: How AMD is Breaking the NVIDIA Monopoly

AMD is positioned to capture market share from NVDA but must deliver on aggressive roadmap. It trades at 49x fwd P/E and 0.7x PEG, targeting 55-58% gross margins and >35% revenue CAGR over 3-5 years.

Company Overview

Advanced Micro Devices (AMD), headquartered in Santa Clara, California, is a global semiconductor, specializing in high-performance computing, graphics, and visualization. Founded in 1969, AMD operates in several key segments: Data Center, Client and Gaming, and Embedded.

The company provides a wide array of products including x86 microprocessors, graphics processing units (GPUs), and artificial intelligence (AI) accelerators. AMD’s product offerings are integrated into accelerated processing units, chipsets, and data center and professional GPUs, under brands like AMD Ryzen, AMD EPYC, and AMD Radeon.

AMD serves OEMs, original design manufacturers (ODMs), system integrators, and public cloud service providers. The company’s products are utilized in various applications such as data centers, gaming consoles, and embedded systems across industries like automotive, healthcare, and communications.

AMD is recognized for its partnerships with leading hyperscale data centers and its role in advancing AI and machine learning capabilities through its Instinct accelerators and ROCm software stack.

Key Business Developments

Data Center segment exploding with MI300X AI accelerator demand

$1B partnership with US Dept of Energy for supercomputers

Acquired Silo AI (AI software expertise) and acquiring ZT Systems (rack-scale solutions)

AMD announced plans for $100B annual data center chip revenue within 5 years

Targeting 55-58% gross margins and >35% revenue CAGR over 3-5 years

Price Action & Technical Context

AMD is currently trading at $213.43 (as of Dec 19, 2025), showing significant volatility and a strong recent rally. The stock has experienced dramatic swings:

Recent surge: From ~$85 in April 2025 to a high of $263 in mid-November, then pulled back to ~$197, and now rebounding to $213

Year-to-date performance: Up substantially from the $120 range in January 2025

Key resistance: The $260-280 zone where it peaked in November

Support levels: $200 psychological level has been tested multiple times recently

The price action shows classic tech stock volatility with AI-driven momentum, but recent pullbacks suggest profit-taking and concern about valuations.

Business Performance

Earnings trajectory shows explosive growth:

Q4 2024: EPS $1.09 (up 42% YoY), Revenue $7.7B (up 24% YoY)

Q1 2025: EPS $0.96 (up 55% YoY), Revenue $7.4B (up 36% YoY)

Q3 2025: EPS $1.20 (up 30% YoY), Revenue $9.2B (up 36% YoY): Beat estimates significantly

All recent quarters have beaten analyst estimates

Analyst Sentiment: Extremely Bullish

The analyst community has dramatically upgraded their stance:

Massive price target increases following Q3 earnings and analyst day (Nov 11-12)

Current targets ranging from $260-$345, with Wells Fargo at $345 (61% upside)

Multiple upgrades throughout 2025 after a rough patch in Q1-Q2

Consensus: AMD is positioned to capture significant AI market share from NVDA

However, there were downgrades in early 2025 (Jan-Apr) when concerns about execution and competition peaked.

Insider Activity: Mixed Signals

CEO Lisa Su has been a consistent seller throughout 2024-2025, but this appears to be on a pre-planned schedule for liquidity (selling ~$10-36M per transaction)

Other executives following similar patterns

Not a red flag: These are structured sales, not panic selling

Commercial insiders like Philip Guido actually bought shares (Feb and May 2025)

Institutional Activity: Accumulating

Institutional investors are aggressively accumulating:

Major additions from UBS ($2.3B added), Two Sigma, SRS Investment Management, Amundi, Bank of America

David Tepper’s Appaloosa took a new 950K share position in Q3

Some hedge funds taking profits (Amazon sold its entire stake), but this is offset by massive new positions

Congress trading:

Marjorie Taylor Greene has been a consistent buyer throughout 2025

Multiple purchases by both parties, with gains ranging 50-130% on recent trades

Options Market: Heavy Activity

The unusual options data shows massive institutional positioning:

Heavy call buying at $220-$280 strikes (bullish bets)

Long-dated call positions (2027-2028) suggesting institutional conviction

Some put protection around $180-$200 (hedging downside)

Premium paid in millions suggests sophisticated money is betting on upside

News Flow: Intensively Positive on AI

Recent headlines are dominated by:

AMD’s aggressive AI roadmap and annual product cadence

Partnerships expanding (OpenAI multi-billion-dollar deal, Microsoft, HPE)

Competitive positioning against NVDA intensifying

France’s first exascale supercomputer using AMD chips

Concerns about China restrictions, but offset by strong US/global demand

Risks Involved

Valuation stretched: Stock has run hard, P/E ratios are elevated for the sector

NVIDIA dominance: NVDA still controls 80%+ of AI accelerator market

Execution risk: AMD must deliver on aggressive roadmap (annual product launches)

China exposure: Geopolitical tensions and export restrictions

Competition intensifying: Hyperscalers building their own chips, Intel fighting back

Memory shortage concerns mentioned by CEO (could constrain AI systems)

Recent selloff in AI stocks (Nov 20-25) shows sector rotation risk

Bottom Line

AMD is in a strong uptrend driven by legitimate AI business acceleration, but the stock is trading at demanding valuations that price in significant future execution. The fundamentals are outstanding, revenue growing 35%+, beating estimates, expanding into AI at scale, and taking share from competitors.

However, the technical setup shows signs of exhaustion near $260, and the stock needs to consolidate recent gains. The $200-215 range appears to be a battleground zone.

This is NOT a sleepy semiconductor play, it’s a high-beta AI infrastructure bet with massive upside potential but equally significant volatility risk. The company is executing well, but expectations are sky-high.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. All opinions expressed are my personal views. Always do your own research and consult with qualified professionals before making investment decisions.

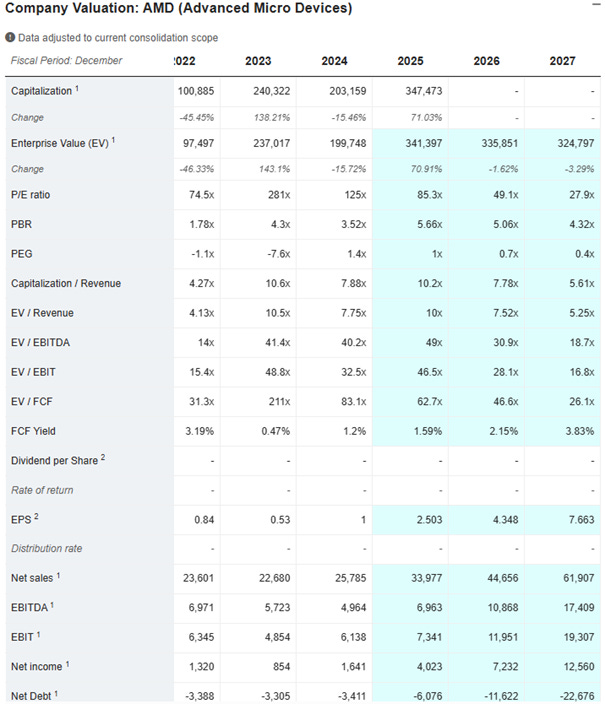

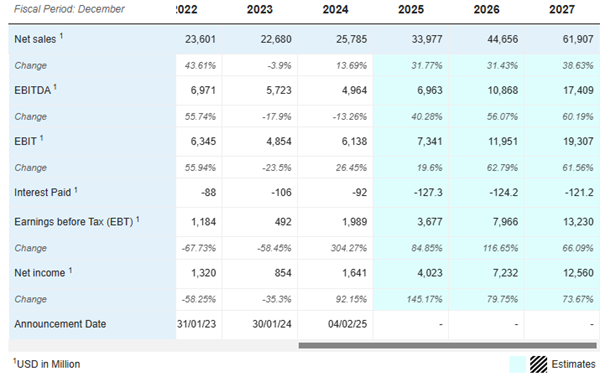

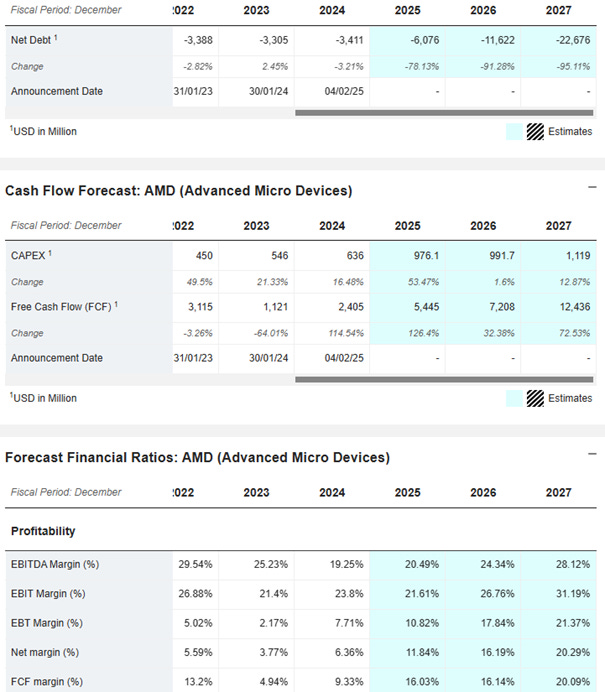

Appendix 1: Financial Projections

Appendix 2: Valuation Metrics