Applied Digital (APLD) Executive Summary: 16x in 6 Months, The Tiny Company Fueling the $8bn Hype

The former crypto host is now AI infrastructure's darling, but a flood of red ink and insider selling makes this a high-stakes gamble.

Company Overview

Applied Digital is the ultimate “pivot story” in the current market. This U.S.-based designer and operator of data center infrastructure is rapidly shedding its legacy as a crypto mining host to become a pure-play provider for High-Performance Computing (HPC) and AI workloads.

The Past: Data Center Hosting Business (286 MW capacity in North Dakota): This is the old, crypto-driven revenue stream.

The Future: HPC Hosting Business (Polaris Forge campus) – This is the new, AI-focused growth engine currently under aggressive development.

In short, Applied Digital is attempting a metamorphosis from Bitcoin miner to AI infrastructure landlord. The market has taken notice, in a massive way.

Price Action & Momentum: The 1,550% Volatility Engine

If you want excitement, Applied Digital delivers. This stock has been a fireworks show:

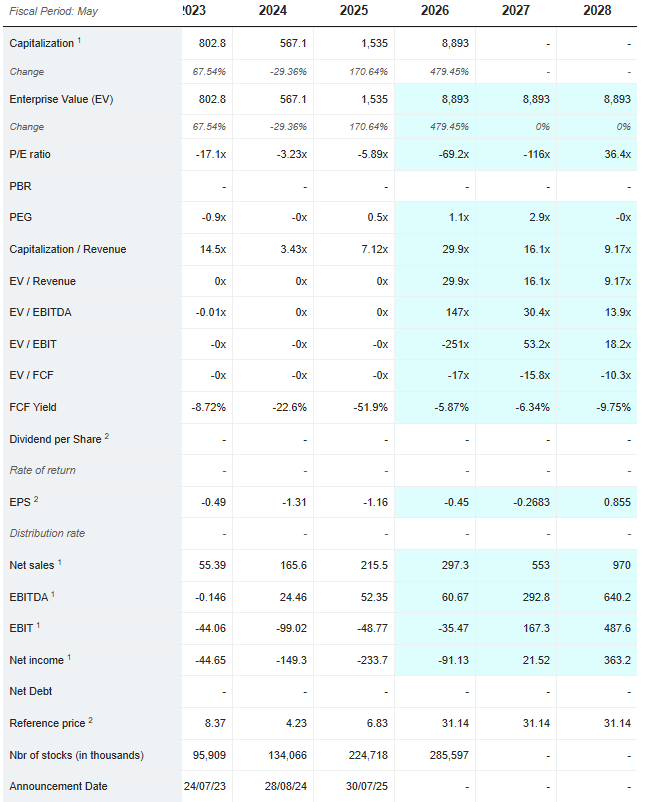

Massive Expansion: The market capitalization exploded from a modest $495M in Q1 2025 to a staggering $8.2B today. That’s a 16x valuation jump in under a year.

The Surge: From a low of $5 in May 2025, the stock has skyrocketed 213% to its current price of $31.14.

The Rollercoaster: The stock is defined by extreme volatility, with the last 150 days seeing swings from the $5 low to a $40 high following an October earnings spike.

The Bull Case and What’s Driving This

AI Data Center Transformation

Secured two 15-year leases totaling 250 MW for Polaris Forge 1 campus

Just announced (Nov 24) Ready for Service on 2nd phase (50 MW) of Building 1 - stock jumped 13%

Partnership with Babcock & Wilcox for $1.5B+ project to deliver 1 gigawatt of power

Total planned capacity: 400 MW across three buildings

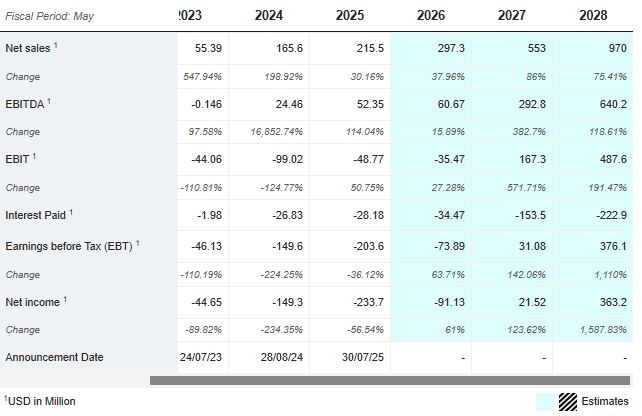

Explosive Revenue Growth

Q1 2026 revenue: $64.2M (up 84% YoY)

Beat estimates by 44% last quarter ($64.2M vs $44.5M expected)

EPS beat: -$0.03 vs -$0.14 expected (78% beat)

Analyst Enthusiasm

All 10 analysts rate it “Buy” - zero holds or sells

Price targets raised dramatically: Roth Capital $43, HC Wainwright $40, Needham $41, JP Morgan $35

Multiple upgrades post-earnings in October

Massive Capital Raise

Just priced $2.35B in senior secured notes (Nov 2025) to fund expansion

Shows confidence in accessing capital markets

Bear Case (Major Red Flags)

Profitability Disaster

Consistently unprofitable: Every quarter shows losses

Negative gross margin in Q4 2025 (-83.5%)

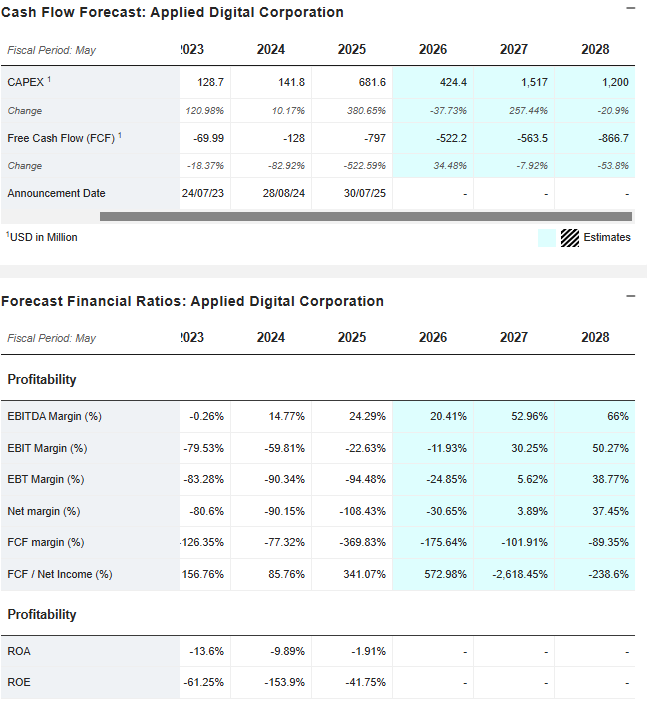

Free cash flow: -$362M in Q1 2026 (burning cash rapidly)

Return on equity: -16.7% (destroying shareholder value)

Financial Weakness

Current ratio: 0.65 (can’t cover short-term obligations)

Debt ratio jumped from 17% to 29% (taking on more debt)

Price-to-sales ratio: 26x (expensive for an unprofitable company)

Execution Risk

Transitioning from mature crypto hosting to unproven AI business

Revenue from AI segment not yet “meaningful”

Single customer concentration in both segments (massive risk)

Supply chain dependencies and tariff exposure

Heavy Insider Selling

CEO Wes Cummins sold $6.1M in September, disposed of 900K+ shares in October

CFO sold $4.8M across multiple transactions

Directors selling consistently (though some awards granted too)

This is NOT on a pre-planned schedule - significant concern

Valuation Disconnected from Reality

Market cap grew from $500M to $8.2B in 6 months on hopes, not profits

Trading at 26x sales while burning cash

No clear path to profitability disclosed

Bottom Line

Applied Digital is the perfect illustration of momentum versus fundamentals.

You have legitimate, market-shifting business wins (Polaris Forge leases) and incredible market hype driving a massive valuation expansion. This is the momentum trade.

But you have an unprofitable, cash-burning, highly leveraged company with single-customer concentration and heavy, un-scheduled insider selling. These are the fundamentals.

If you’re buying Applied Digital at $31, you are making a high-risk, speculative bet that AI infrastructure demand will materialize fast enough and large enough to justify an $8 billion valuation for a company that is currently losing money and generating only about $230 million in annualized revenue.

The technical setup shows strength, but the margin for error is zero. One execution miss, one delayed construction phase, or one lost customer could trigger a brutal and swift correction.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. All opinions expressed are my personal views. Always do your own research and consult with qualified professionals before making investment decisions.

Appendix 1: Financial Projections

Appendix 2: Valuation Metrics

Applied Digital (APLD) reported a massive 139% revenue surge to $126.6 million for fiscal Q3 2026, significantly beating analyst estimates driven by intense demand for its AI-ready data centers. While the company saw a widened GAAP net loss of $100.9 million due to heavy infrastructure investment and a cloud-related impairment charge, it achieved a surprise adjusted net income of $0.09 per share. Operationally, the company has broken ground on its massive 430 MW Delta Forge 1 AI Factory and secured a $100 million financing facility to fuel further expansion. CEO Wes Cummins noted that the current operational capacity is just a fraction of the company's contracted pipeline, signaling significant "earnings power" ahead. Despite the strong revenue beat, shares dipped in extended trading as investors balanced the rapid growth against rising capital expenditures.