Broadcom (AVGO) Executive Summary: Is This a Buying Opportunity or the Start of a Meltdown?

The 15% decline serves as a sobering reminder of the risks inherent in overextended momentum plays, especially with insider selling adding a layer of bearish sentiment

Company Overview

Broadcom (AVGO) headquartered in Palo Alto, California, designs, develops, and supplies a wide range of semiconductor devices and infrastructure software solutions.

Broadcom’s semiconductor products are integral to applications such as enterprise and data center networking, AI networking, home connectivity, telecommunications, smartphones, and data center servers. These products include Ethernet switching, custom silicon solutions, RF front-end modules, and fiber optic components.

The Infrastructure Software segment offers solutions that help enterprises manage and secure IT environments, supporting applications across mainframe, cloud, and hybrid platforms.

Broadcom’s strategic acquisitions, like the VMware merger, have enhanced its product portfolio, allowing it to address complex IT infrastructure challenges.

The AI Story

AVGO’s AI custom chip business is exploding:

$73B AI backlog disclosed post-earnings

Partners include OpenAI, Google (GOOGL), Meta (META)

Secured 50% of Samsung’s HBM output for Google TPU chips

AI revenue hit $6B in Q4 alone

Q1 2026 guidance: $19.1B revenue (above $18.3B estimate)

The company is pivoting from networking silicon to AI custom chips, a strategic shift that’s working, but comes with execution risk.

Price Action & Technical Context

AVGO is experiencing significant technical weakness. The stock crashed from $412.9 (Dec 10) to $324.6 (Oct 10), a brutal 15% drop in 5 days following Q4 earnings on Dec 11. Currently trading at $341.3 (down from recent highs).

The 10-for-1 stock split executed in July 2024 makes historical comparisons tricky, but the recent selloff is severe by any measure. The stock hit all-time highs above $410 before earnings, then plummeted despite beating estimates.

Earnings Overview

Recent earnings have been spectacular on paper:

Q4 2025 (Dec 11): EPS $1.95 vs $1.72 est (+13.4% beat), Revenue $18.0B vs $17.5B est (+3% beat)

Q3 2025: EPS $1.69 vs $1.54 est (+9.7% beat), Revenue $16.0B vs $15.8B est

Consistent beats for 8 straight quarters with YoY EPS growth of 27-45%

The problem: Q1 2026 guidance spooked markets. Management warned of margin pressure and highlighted 2026 tax hikes that could overshadow AI growth. This cautious tone triggered the selloff despite record AI revenue.

Valuation Overview

Market cap: $1.6 trillion (peak was higher)

Fwd P/E ratio: 44.7x, elevated compared to 31.4x sector median

Fwd P/S ratio: 24.1x, also at multi-year highs

Net profit margin: 26-37% (strong but declining from Q1 peaks)

Free cash flow: $7.4B (Q3), solid cash generation

The valuation reflects AI euphoria, but the recent P/E expansion looks unsustainable given margin pressure warnings.

Analyst Sentiment

48 analyst upgrades since September with zero downgrades. Recent price target increases:

Post-earnings (Dec 12): Targets raised to $450-500 range

Keybanc: $460 → $500

Bank of America: $460 → $500

Barclays: $450 → $500

JP Morgan: $400 → $475

Consensus: Strong AI tailwinds justify premium valuation despite near-term margin concerns. Analysts see this pullback as temporary.

Insider & Institutional Activity

Insiders selling heavily:

CEO Hock Tan sold $50M+ in September (two $50M transactions on Sep 10)

Henry Samueli (Director) sold $125-128M in June, Sept, Dec

Multiple executives disposing of stock throughout 2025

This is not bullish but could be scheduled selling. The volume and frequency raise eyebrows.

Congress: Notable purchases by Nancy Pelosi ($1M-5M in June) and Michael McCaul (multiple buys). They’re net buyers despite volatility.

Hedge funds (13F data): Mixed. Major adds from Point72, Amundi, CIBC. Major trims from Bank of America (-$1.7B), Morgan Stanley (-$239M). Net institutional sentiment is cautious.

Bull Case:

Broadcom securing Microsoft AI chip discussions (Dec 8)

Google TPU chips reportedly 40% cheaper to run than NVDA’s (bullish for AVGO partnership)

Expanding private cloud business

Bear Case:

Oracle delays in data center projects spooked broader AI infrastructure stocks

Margin pressure warnings overshadowing revenue growth

Semiconductor sector rotation out of “expensive” AI names

Valuation compression: Fwd P/E of 44.7x is elevated, vulnerable to multiple contraction

Customer concentration: Heavy reliance on 2-3 hyperscalers (Google, Meta, OpenAI)

Margin pressure: Management flagged this explicitly

Execution risk: Pivoting from networking to custom AI chips is complex

Competition: NVDA, AMD, MRVL all competing in AI infrastructure

Bottom Line

Broadcom is a high-quality AI infrastructure play with exceptional revenue growth, but the stock is overextended and vulnerable. The post-earnings crash reflects reality catching up to valuation, even great earnings can’t justify 44.7x+ Fwd P/E forever when margins are under pressure.

The $324-$340 range could be support, but this chart looks damaged. The rapid 15% drop after earnings is a classic bull trap, longs who bought the breakout above $400 are underwater. Insider selling adds to the bearish case. If you own this, the risk/reward is skewed negative short-term.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. All opinions expressed are my personal views. Always do your own research and consult with qualified professionals before making investment decisions.

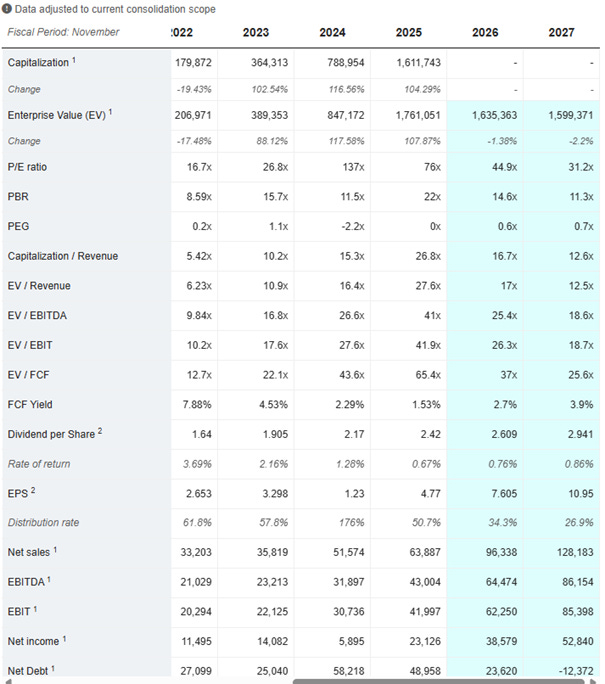

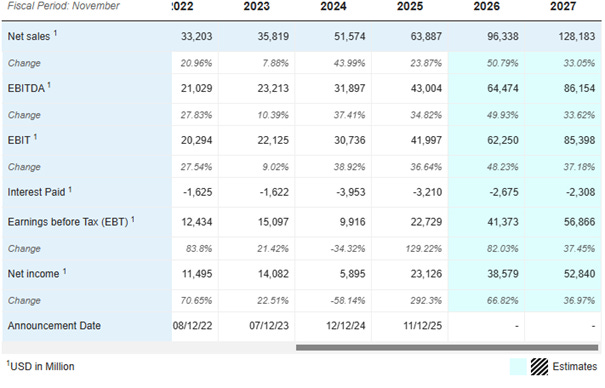

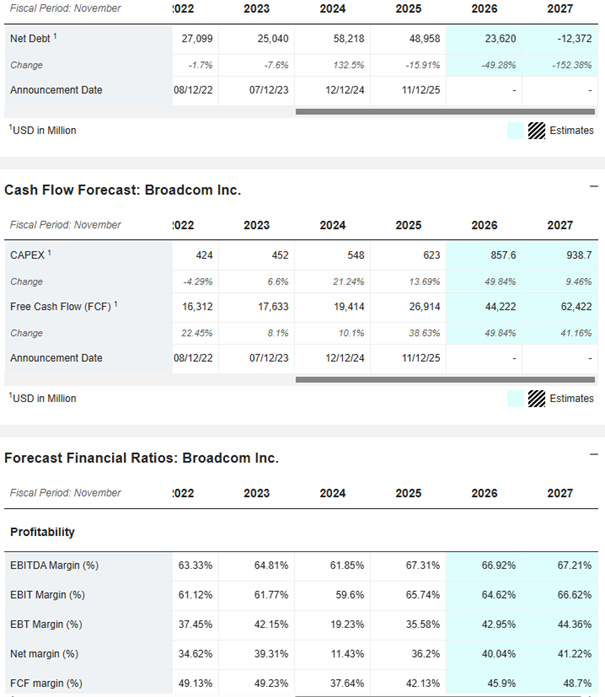

Appendix 1: Financial Projections

Appendix 2: Valuation Metrics