CoreWeave (CRWV) Executive Summary: The AI Cloud Poster Child Is Cut in Half, What's Next?

CRWV has been virtually halved from its summer high, signaling a dramatic shift in market sentiment. CRWV remains a battleground stock where the technical distress outweighs the fundamental strength.

Company Overview

CoreWeave the specialized AI cloud infrastructure provider known as “The Essential Cloud for AI,” has become a key focal point in the debate over the sustainability of the AI boom. With a market capitalization of $38.4 billion, the company boasts immense growth but has recently seen its stock price enter a severe, punishing downtrend.

CoreWeave’s business model is centered on being a specialized, GPU-first AI cloud infrastructure provider. The company’s strategy is built on quickly deploying cutting-edge NVIDIA GPUs (like H100 and Blackwell) in its high-density data centers to power demanding AI and ML workloads.

Revenue and Financial Visibility:

Primary Revenue: Dominated by long-term committed contracts (typically 2-5 year, “take-or-pay” agreements) with major clients like OpenAI, Meta, and Microsoft. This structure provides exceptional revenue visibility and a massive, reliable Revenue Backlog (RPO), which is crucial for financing the company’s significant capital expenditure (CapEx).

Secondary Revenue: Includes flexible, Usage-Based Services for GPU compute, storage, and networking on the proprietary CoreWeave Cloud Platform.

CoreWeave maintains its market leadership through three key differentiators against general-purpose hyperscalers:

GPU Specialization: Its infrastructure is purpose-built and optimized for GPU-intensive workloads, delivering superior performance (higher efficiency and throughput) and a lower Total Cost of Ownership (TCO) for clients focused on large-scale AI model training and inference.

Strategic NVIDIA Partnership: An extremely close relationship with NVIDIA ensures early and massive access to the latest GPU technology, allowing CoreWeave to rapidly bring new, high-demand infrastructure to market ahead of competitors.

Scaling Execution: The company has demonstrated the capability to contract for and rapidly deploy vast amounts of power capacity (Gigawatts) and assemble large, tightly-coupled GPU clusters, which are non-negotiable for building the largest foundation models.

The Anatomy of a Stock Collapse

The stock has been virtually halved from its summer high, signaling a dramatic shift in market sentiment.

Peak to Trough: The stock plummeted 56% from its peak of $173.35 on June 30 to its current price of $76.03 on December 2, erasing over half its value in just five months.

The November hit: The decline accelerated post-earnings, losing an astonishing 46% in just over a month

Technical Breakdown: The stock has failed to hold successive major support levels, breaking below $100$, then $90$, and $80$. It is now aggressively testing the critical $75-$76 area, a level last seen shortly after its IPO.

Volume Spike: The recent volatility is confirmed by significantly elevated trading volume (24 - 41 million shares per session), nearly double the mid-summer range, suggesting a fierce battle between panic selling and aggressive bargain hunting.

Fundamental Conflict: Backlog vs. Bottleneck

The irony of CoreWeave is the stark divergence between its fundamental metrics and its stock price. The underlying demand for its GPU-accelerated computing services is explosive, yet execution risks have overshadowed this success.

Record-Breaking Growth…

The triple-digit revenue growth confirms CoreWeave’s dominance in a high-demand niche. Furthermore, the company has secured unprecedented future revenue:

The total revenue backlog nearly doubled in Q3 alone, reaching a staggering $55.6 billion.

The firm successfully expanded its credit facility from $1.5 billion to $2.5 billion, demonstrating strong institutional faith in its long-term potential.

New partnerships, such as the $1.17 billion deal with VAST Data for high-performance storage, continue to expand its infrastructure ecosystem.

...Meets Execution Risk

The major headwind is the critical execution issue reported on November 10:

The company was forced to lower its FY2025 guidance from $5.15 - 5.35$ to $5.05 - 5.15$.

The cause was explicitly attributed to delays at third-party data centers, specifically issues related to Core Scientific that are affecting 590MW of leased capacity.

This guidance cut crystallized the bear case: CoreWeave’s success is dependent on its ability to rapidly secure, build out, and deploy physical infrastructure. The delay highlights that the physical supply chain and power availability, not customer demand and is the new bottleneck in the AI race.

Wall Street and The Narrative Shift

Following the guidance cut, Wall Street turned sharply cautious, contributing significantly to the stock’s freefall:

Analyst Deterioration: Post-November 11, multiple firms downgraded the stock and slashed price targets. J.P. Morgan downgraded CRWV to Neutral with a price target of $110 (down from Overweight), while Loop Capital cut its target from $165 to $120.

Valuation Spread: Consensus targets have fragmented wildly, ranging from a bearish $36 (D.A. Davidson’s Sell rating) to an extremely bullish $180 (HC Wainwright), showing deep disagreement on the stock’s true value.

Bear Case Intensifies: The market narrative has shifted from celebrating AI infrastructure growth to questioning the entire sector’s valuation. Headlines suggesting the “AI Bubble Is Bursting” and warnings from analysts of a “wild, lumpy, volatile ride” have driven broad sector rotation and skepticism.

Key Investor Sentiment Signals

Options Activity: The options market reflects extreme uncertainty. Heavy volume in both calls and puts, particularly long-dated 2027-2028 strikes, shows large investors are both hedging against the downside (put buying) and betting on a massive future rebound (long-term call buying).

Institutional Faith: Despite the selloff, high-profile institutional investors are stepping in. Cathie Wood’s ARK Invest notably purchased $32 million worth of stock on November 24, suggesting conviction that the long-term growth thesis outweighs the near-term execution issues.

The Bottom Line: Opportunity or Trap?

CoreWeave presents one of the most compelling risk/reward profiles in the current market.

The bull case: Massive backlog ($55B+), triple-digit revenue growth, expanding partnerships, and sector-leading position in AI cloud infrastructure.

The bear case: Execution risks are materializing, capital requirements are enormous, competition is fierce, profitability remains distant, and the market is questioning whether AI infrastructure demand justifies current valuations.

The current price of $76.03 is testing the lowest technical support established since the IPO-related selloff in May.

Risk: If this support breaks, the next major downside target is the $65-70 zone.

Reward: A successful defense of the $75-76 level, coupled with positive operational updates, could spark a significant relief rally toward $90-100.

However, the severe downtrend will only be considered truly broken if the stock can decisively reclaim the $110+ level, which corresponds to the lower end of the previous analyst price targets. Until then, CRWV remains a battleground stock where the technical distress outweighs the fundamental strength.

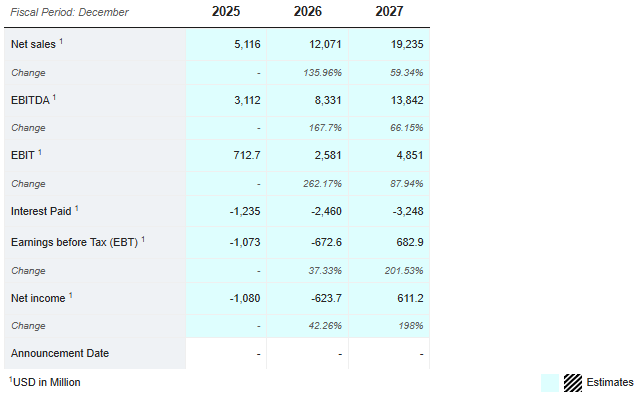

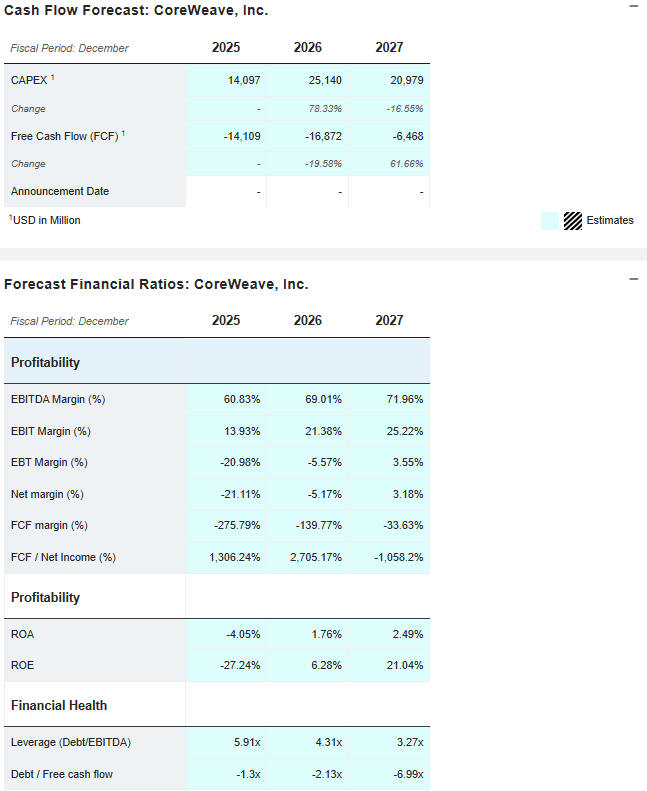

Appendix 1: Financial Projections

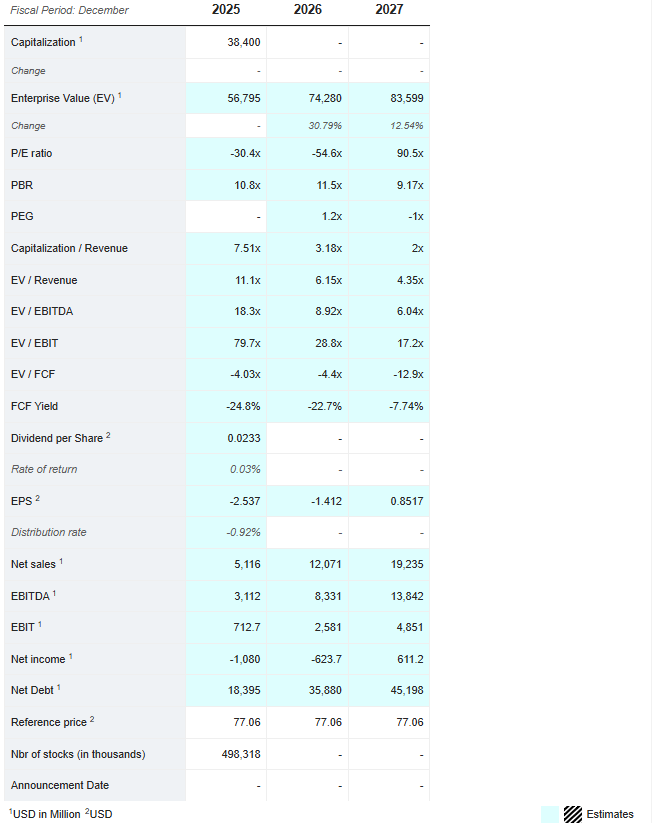

Appendix 2: Valuation Metrics

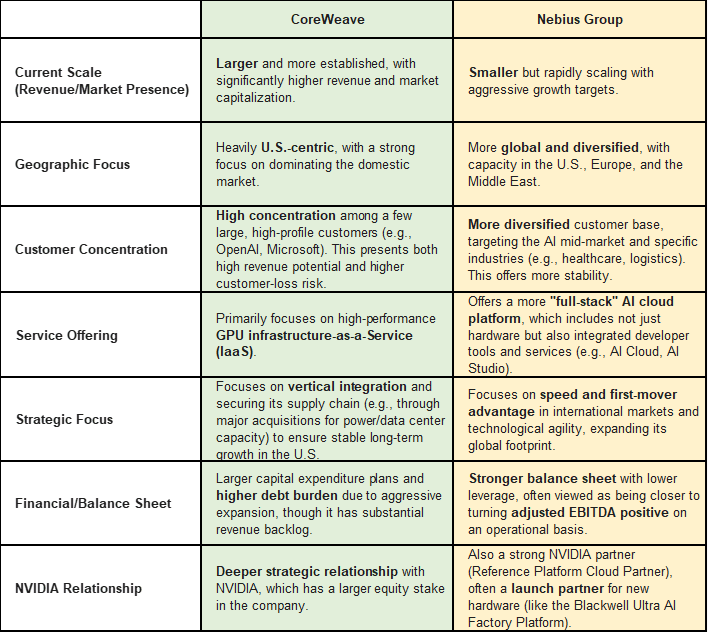

Appendix 3: Competitive comparison with Nebius

CoreWeave and Nebius Group are direct competitors in the high-growth market of specialized AI-focused cloud infrastructure, often referred to as “neocloud” providers. They both offer data center services powered by high-performance NVIDIA GPUs for compute-intensive workloads like AI model training and inference, positioning themselves as agile alternatives to traditional hyperscalers (like AWS or Azure). While their core service is similar, their business strategies and market profiles exhibit notable differences: