Deep Dive: Microsoft (MSFT): Full Valuation Case & Monte Carlo Simulation

Institutional grade research on Microsoft with catalysts to watch and actionable insights for investing

Company Overview

Microsoft, founded in 1975 and headquartered in Washington, is a global leader in software, services, devices, and solutions. The company operates through several segments: Productivity and Business Processes, Intelligent Cloud, and Personal Computing.

Microsoft’s Productivity and Business Processes segment offers widely used products such as Microsoft 365, which includes Office, SharePoint, and Microsoft Teams, as well as LinkedIn and Dynamics 365.

The Intelligent Cloud segment is known for its Azure cloud services, GitHub, and enterprise solutions like SQL Server and System Center.

Microsoft’s Personal Computing division encompasses Windows operating systems, Surface devices, Xbox gaming consoles, and Bing search services.

The company sells its products through various channels, including OEMs, distributors, resellers, and direct online sales.

Microsoft is actively involved in AI advancements and has a partnership with Richtech Robotics Inc. to develop AI capabilities in robotics.

Price Action & Technical Context

Microsoft is currently trading at $423.37 (as of Feb 2, 2026), sitting in a significant downtrend. The stock has plunged approximately 13% from recent highs around $489 in early January. This represents the worst single-day drop since March 2020 following the Q2 earnings report on Jan 28.

Key technical levels:

Weekly chart shows a breakdown from the $470-490 consolidation zone

Currently testing support around $420-425

Major support below at $390-400 (April 2025 lows)

The stock has made a series of lower highs and lower lows since late October 2025

Earnings Catalyst: What went wrong

Q2 FY2026 Results (Jan 28):

EPS: $4.14 (beat est. $3.86 by 7.3%)

Revenue: $81.3B (beat est. $80.3B by 1.3%)

Azure growth: 31% (guidance was 37-38% for Q3)

Despite beating estimates, the stock crashed 10%+ after hours. Why? AI monetization concerns and capital expenditure anxiety:

Azure growth deceleration - While still strong at 31%, it’s below expectations

Massive CapEx with unclear ROI timeline - Investors want proof the AI bet is paying off

Q3 guidance disappointment - Azure growth of 37-38% expected vs. higher hopes

Operating margin pressure - Expected to decline YoY in Q3 due to AI infrastructure costs

CFO Amy Hood’s comments about AI demand and capacity constraints weren’t enough to calm concerns about when the massive infrastructure spending will translate to proportional revenue growth.

Earnings Trajectory

The earnings show consistent double-digit YoY growth, but the rate is what matters:

Q2’26: +28% YoY (EPS $4.14)

Q1’26: +23% YoY (EPS $4.13)

Q4’25: +24% YoY (EPS $3.65)

Q3’25: +18% YoY (EPS $3.46)

Revenue growth averaging 15-18% YoY, which is excellent for a $3.2T company, but investors expected more explosive AI-driven growth given the investment scale.

Growth Potential Assessment

Revenue Growth Drivers:

Strengths (Supporting Higher Valuation):

Azure AI leadership

Deep OpenAI partnership, comprehensive AI platform

Copilot ramping - 50M seats growing 75% YoY (massive TAM)

Enterprise moat - Sticky customer base, high switching costs

Diversified portfolio - Not dependent on single product line

Financial strength - Can self-fund AI investments without financial stress

Concerns (Pressure on Valuation):

CapEx explosion - $60B+ annually with unclear near-term ROI

Azure deceleration - Growth slowing from 40%+ to low 30%s

Margin pressure - Operating margins declining in near term

AI monetization timing - Revenue lagging investment by 12-24 months

Competition intensifying - AWS, Google, emerging AI players

Historical Growth Context

2021-2023: 15-18% revenue growth, 35x+ P/E (AI hype phase)

2023-2025: 16-18% revenue growth, 28-33x P/E (growth delivery)

2026E: 13-15% revenue growth, 24-28x P/E (investment phase)

Key Question: Can MSFT maintain 15%+ growth while absorbing massive AI infrastructure costs?

Analyst Sentiment: Turning Cautious

Massive price target cuts post-earnings:

Wells Fargo: $700 → $630 → $615

Evercore: $640 → $580

Wedbush (Dan Ives): $625 → $575

Bank of America: $640 → $520 (dramatic cut)

UBS: $650 → $600

All analysts maintain Buy ratings, but the magnitude of cuts reveals concern about the AI investment payback timeline. The average target is now around $600, implying ~40% upside, but down significantly from prior expectations.

Insider & Government Activity

Insiders: Mostly routine stock awards and scheduled selling. Notable:

CEO Satya Nadella sold $75M in September (pre-planned)

Regular insider selling patterns don’t signal panic

Congress: Mixed activity with both purchases and sales. Notable:

Senator Mullin (R) purchased $250-500K in November

Multiple small transactions from both parties

Overall neutral signal

Options Flow: Great Uncertainty

Post-earnings options activity shows massive hedging and positioning:

Heavy PUT buying at $420-430 strikes (downside protection)

Large CALL buying at $430-450 (recovery bets)

Unusual $430 straddles suggest expectation of continued volatility

Multi-million dollar spreads indicating institutional repositioning

The options market is pricing in continued volatility with no clear directional consensus.

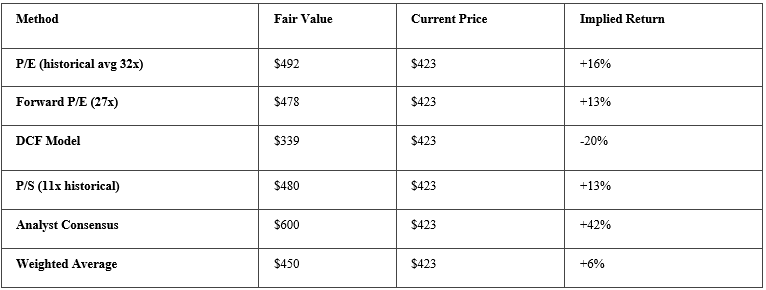

Valuation Summary

For detailed calculations, please see the appendices.

Here’s why this is not a screaming buy despite the selloff:

DCF Model Shows 25% Premium - Conservative cash flow analysis suggests fair value around $340-360, meaning current price already bakes in significant growth optimism

P/E Multiple is Reasonable, Not Cheap - At 27.5x trailing and 23.9x forward, MSFT is trading in line with its growth profile. It’s not expensive, but it’s not a bargain either.

Growth is Decelerating - From 25%+ to 15% expected, which doesn’t justify premium multiples without AI monetization proof

Near-Term Headwinds - Operating margin compression, Azure deceleration, and CapEx pressure are real issues that will persist for 2-4 quarters

Relative Performance Collapse - Dropping from 70th to 15th percentile vs S&P 500 suggests fundamental re-rating in progress

Scenario Analysis

Bull Case Analysis: Fair Value $550-600

Assumptions:

Azure growth re-accelerates to 35%+

Copilot adoption exceeds expectations (100M+ seats by FY27)

AI monetization validates infrastructure spending

Operating margins stabilize at 43-45%

Multiple expansion to 32x P/E

Target: $17.69 forward EPS × 32x = $566

Base Case Analysis: Fair Value $450-480

Assumptions:

Azure growth stabilizes at 30-33%

Steady Copilot adoption (60-70M seats)

AI revenue growth meets but doesn’t exceed expectations

Margins compress to 40-42% near term

Fair multiple: 27-28x P/E

Target: $17.69 × 27x = $478

Bear Case Analysis: Fair Value $350-380

Assumptions:

Azure growth declines to mid-20%s

AI investment ROI disappoints

Competitive pressure intensifies

Margin compression worsens

Multiple contraction to 20-22x P/E

Target: $17.69 × 21x = $371

What Could Change the Thesis?

Catalysts for Upside:

Azure growth re-accelerates to 35%+ in Q3/Q4

Copilot adoption inflection (75M+ seats announced)

Management demonstrates clear AI ROI in numbers

Operating margins stabilize and improve sooner than expected

Catalysts for Downside:

Azure growth declines to mid-20%s

Copilot adoption disappoints expectations

CapEx guidance increases further without revenue justification

Major competitive losses to AWS/Google in AI space

Microsoft at $423 is priced for moderate optimism - not cheap enough to be a value play, not expensive enough to be obviously overvalued. The market is saying: “Show me the AI monetization numbers, then we’ll pay you more.”

If you believe AI infrastructure spending will generate strong returns within 12-24 months, current price offers ~15-20% upside to $480-500 range.

If you’re skeptical about near-term AI monetization, there’s 15-20% downside risk to $340-360 range.

It’s a show-me story where Microsoft needs to prove the AI investments are translating to revenue growth and margin expansion. The valuation is fair for what they’ve delivered, but needs proof points to expand from here.

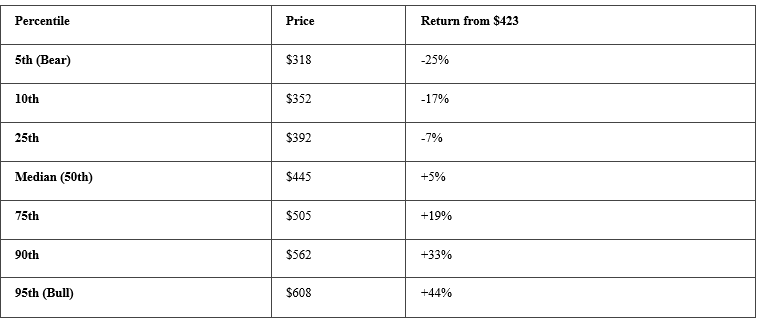

Monte Carlo Results

The simulation reveals limited upside, meaningful downside:

Median upside: +5% (to $445)

Potential downside: -25% (5th percentile at $318)

Risk/Reward ratio: 1:1.3 (mediocre)

Standard deviation of $74 means:

68% confidence interval: $374-522 (±16% from median)

95% confidence interval: $300-596 (±33% from median)

This wide range reflects genuine uncertainty about AI monetization timing.

The correlation analysis shows Azure growth explains nearly 80% of price variance. This means:

If Azure surprises positively (>35%), stock easily hits $520-550

If Azure disappoints (<28%), stock falls to $340-370

Current price assumes Azure performs exactly in-line with lowered expectations

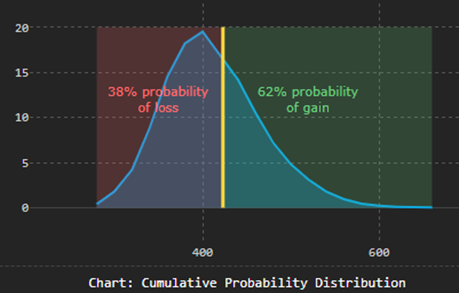

The probability of loss (38%) is uncomfortably high for a quality mega-cap. Compare to typical value investments where you want <20% probability of loss.

All in all, Microsoft at $423 is Fairly valued with a slight downside skew

Median outcome: $445 (+5%)

Mean outcome: $448 (+6%)

Risk-adjusted return: Mediocre (Sharpe ~0.25)

Probability of loss: 38% (too high)

Asymmetry: Downside risk exceeds upside potential

Is MSFT undervalued?

62% probability of some gain (but likely small)

Only 25% probability of >20% gain

38% probability of loss

Break Even Analysis

What needs to happen for MSFT to justify current $423 price?

Required conditions (at minimum):

Azure growth: ≥30% sustained

Operating margin: ≥39%

Overall revenue growth: ≥13%

Market multiple: ≥26x forward P/E

Current market expectations embedded in $423:

Azure will stabilize at 31-33% growth

Margins will bottom at 38-40% then recover

AI investments will show ROI within 12-18 months

No major competitive losses

For price to move significantly higher ($500+):

Azure needs to re-accelerate to 35%+

Copilot needs to hit 75M+ seats by year-end

Operating margins need to surprise to upside (41%+)

Market needs to regain confidence in AI timeline

Risk-Adjusted Return Profile

E(Return) = Σ(Probability × Outcome)

Bear scenario (30%): -14% × 0.30 = -4.2%

Base scenario (50%): +6% × 0.50 = +3.0%

Bull scenario (20%): +28% × 0.20 = +5.6%

Expected Return: +4.4%

Risk-Adjusted Return (Sharpe-like ratio):

Expected return: 4.4%

Standard deviation: 17.5%

Sharpe ratio: 0.25 (below 1.0 = not compelling)

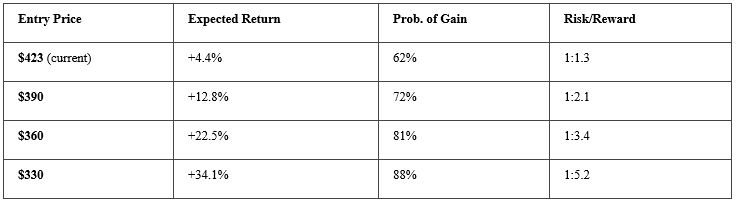

What Price would MSFT be undervalued?

Running the simulation with lower entry points:

Sweet spot for value entry: $360-380 range

This is where probability shifts strongly in your favor

Expected return exceeds 15%

Risk/reward becomes compelling (>2:1)

The Bear Case

The market is punishing MSFT because:

CapEx exploding faster than revenue - AI infrastructure spending is front-loaded

Azure growth decelerating - From 40%+ to low 30%s

Margin compression - Operating margins declining due to datacenter investments

AI monetization unclear - Where’s the ROI on hundreds of billions in AI spending?

Software sector weakness - Broader rotation out of high-multiple tech

Valuation reset - Trading at high multiples with growth slowing

The Bull Case

Despite the selloff, bulls argue:

Early innings of AI adoption - Enterprise AI transformation is multi-year

Copilot ramping - 50M seats growing rapidly, massive TAM ahead

Azure leadership maintained - Still #2 cloud provider with AI differentiation

Diversified portfolio - Not just an AI play; strong core businesses

Financial strength - Massive cash flow funds AI investments without distress

Analyst consensus still Buy - Price targets imply 40%+ upside

Based on the Monte Carlo simulation, the bull case ($520-620 range) requires multiple positive catalysts to materialize. Let’s analyze each potential catalyst with probability assessments and timing.

1. Azure Growth Re-Acceleration to 35% +

What it means: Q3 or Q4 Azure growth surprises to the upside, beating the guided 37-38% and hitting 38-42% range

Why it matters:

Azure growth explains 78% of stock price variance (per Monte Carlo)

Would validate that AI demand is real and accelerating

Proves infrastructure investments are translating to revenue

Current signals:

Microsoft exec said Q3 Azure guidance is 37-38% (vs Q2 actual 31%)

CFO Amy Hood mentioned capacity constraints limiting growth

But warned margins will compress in Q3

Competitive pressure from AWS/Google intensifying

Probability assessment: 35%

Reasoning:

Management guided 37-38% for Q3, implying they see sequential improvement

Capacity additions coming online could unlock pent-up demand

BUT guidance was lowered post-earnings, suggesting caution

Historical pattern: When MSFT guides conservatively, they often beat by 1-2 points

Timeline:

Next catalyst: Q3 earnings (April 30, 2026)

Stock reaction if realized: +15-25% spike on earnings beat

Conditional probability chain:

If Q3 Azure hits 38%+: 70% chance stock moves to $500+

If Q4 confirms acceleration (40%+): 85% chance stock hits $550+

2. Copilot Adoption Inflection (75M+ Seats)

What it means: Microsoft announces Copilot seats grew from 50M to 75M+ within 6 months, with strong monetization metrics

Why it matters:

Copilot is the primary AI monetization vehicle

Demonstrates enterprises are willing to pay premium for AI productivity

Directly impacts revenue and justifies AI CapEx spending

Creates defensible moat (users become dependent on AI workflows)

Current signals:

Q2 reported: 50M paid Copilot seats

Growing 75% YoY (very strong growth rate)

GitHub Copilot showing “strong growth across all paid” offerings

Franklin Templeton just launched AI-powered hub with MSFT

4.7M consumer Copilot subscribers (small but growing)

No specific revenue breakdown or ARPU disclosed

Probability assessment: 45%

Reasoning:

Current trajectory: 50M seats growing 75% YoY = ~87M seats in 12 months

BUT that’s 75% YoY, not quarter-over-quarter

Enterprise adoption cycles are accelerating but still conservative

Competitors (Google Gemini for Workspace, Amazon Q) are ramping

Math check:

50M seats at ~$30/month = $1.5B monthly run rate = $18B annual

75M seats = $27B annual Copilot revenue

Each 10M incremental seats = ~$3.6B revenue

This would be massively accretive to margins once infrastructure is built

Timeline:

Next catalyst: Q3 earnings update (April 30)

Major inflection point: Q4 earnings (July 29) - full year data

Stock reaction if realized: +12-18%

Conditional probability:

If Copilot hits 70M+ by Q3: 60% chance stock reclaims $480+

If management breaks out Copilot revenue separately: 75% chance positive reaction

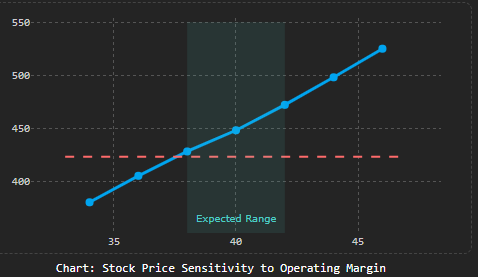

3. Operating Margin Surprise (41%+ vs. 38-40% expected)

What it means: Microsoft demonstrates better cost controls or faster AI monetization, leading margins to surprise to upside

Why it matters:

Each 1% margin improvement = ~$17-20 stock price impact (per sensitivity analysis)

Would prove AI spending isn’t destroying profitability

Reduces bear case concerns about unsustainable CapEx

Current signals:

Management guided Q3 margins DOWN slightly YoY

CapEx remains elevated (datacenter buildout continues)

Memory chip shortage driving costs up

Microsoft rolling out custom Maia 200 chips (cost savings potential)

Efficiency initiatives mentioned by CEO

Probability assessment: 25%

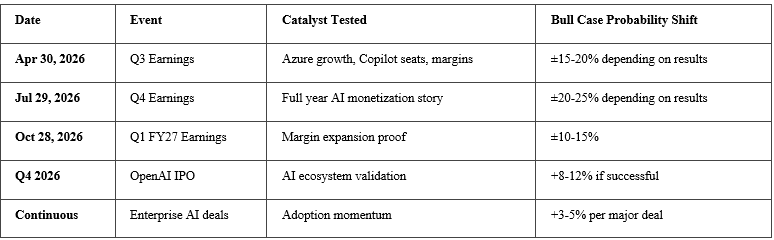

Critical dates to Watch

Bull Case Summary

Trading Implications

For long-term investors (1+ year horizon)

Current price ($423) offers mediocre risk/reward:

Expected return: +4-6%

Too much downside risk for meager upside

Better entry: $380-400 range (75th percentile outcome becomes base case)

For Value Investors

Wait for DCF fair value:

Target entry: $340-360 (DCF fair value with margin of safety)

This gives 20%+ upside to base case, 40%+ to bull case

Only 15% probability simulation goes lower

For Growth Investors

Current price is acceptable IF you believe:

Azure will beat expectations (>33%)

Copilot adoption will accelerate

AI monetization happens sooner than consensus

Risk: 35-40% chance you’re down 10-20% before being right

For Momentum Traders

Avoid until technical confirmation:

Stock needs to reclaim $460-470 to signal bottom is in

Relative strength needs to recover above 30th percentile

Current downtrend remains intact

Bottom Line

Microsoft is currently navigating a “Growth at a Reasonable Price” (GARP) identity crisis, but don’t let the noise fool you: the company is doing exactly what a market leader must. Management is aggressively front-loading capital expenditures investing in the datacenters, GPUs, and power infrastructure necessary to dominate the next decade of compute. While these immediate costs have created a temporary timing mismatch against slower enterprise adoption cycles, this isn’t a fundamental flaw in the business model it’s a necessary bridge to the next leg of trillion-dollar growth.

The current margin pressure is a short-term side effect of long-term ambition. This is the “shakeout” phase where expectations are finally meeting the reality of infrastructure scaling, providing a disciplined entry point for those who believe in the Azure re-acceleration story.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. All opinions expressed are my personal views. Always do your own research and consult with qualified professionals before making investment decisions.

Appendix 1: Earnings Based Valuation

TTM PE multiple

Based on the last 4 quarters of earnings:

Q2’26: $4.14

Q1’26: $4.13

Q4’25: $3.65

Q3’25: $3.46

TTM EPS = $15.38

Current P/E Ratio = $423.37 / $15.38 = 27.5x

Forward PE multiple

Projecting next 4 quarters (Q3’26-Q2’27) with conservative growth assumptions:

Historical growth: 20-28% YoY

Conservative forward estimate: 15% growth

Forward EPS estimate: $17.69

Forward P/E = $423.37 / $17.69 = 23.9x

Peer Comparison

Historical tech sector P/E multiples:

Microsoft historical average (2020-2025): 30-35x

Mega-cap tech peers current: 25-32x range

S&P 500 average: ~18-20x

Analysis: At 27.5x trailing and 23.9x forward, MSFT is trading:

Below its 5-year average of 32-33x

In line with mega-cap tech peers

Premium to S&P 500 but justified by superior growth and margins

PEG Ratio

PEG = P/E / Growth Rate

Using forward P/E of 23.9x and expected growth:

Optimistic scenario (20% growth): PEG = 23.9 / 20 = 1.20x

Base case (15% growth): PEG = 23.9 / 15 = 1.59x

Conservative (12% growth): PEG = 23.9 / 12 = 1.99x

MSFT is in the fairly valued to slightly overvalued range depending on growth assumptions. The market is pricing in ~15% growth, which is conservative given historical performance.

Appendix 2: Discounted Cash Flow Analysis

Revenue & Free Cash Flow Projection: Based on Q2’26 revenue of $81.3B (annualized ~$325B):

5-Year Revenue Projection:

FY26: $325B (baseline)

FY27: $365B (+12% growth)

FY28: $402B (+10%)

FY29: $434B (+8%)

FY30: $460B (+6%)

Free Cash Flow (FCF) Assumptions:

Historical FCF margin: 35-40% of revenue

Near-term pressure from AI CapEx: 30% margin

Improving to 35% by FY30

Projected FCF:

FY26: $97.5B

FY27: $109.5B

FY28: $120.6B

FY29: $139.0B

FY30: $161.0B

Assumptions:

Discount rate (WACC): 9% (reflecting risk-free rate + equity premium)

Terminal growth rate: 3.5%

Shares outstanding: ~7.45B

Present Value of FCF (FY26-FY30):

Year 1: $97.5B / 1.09 = $89.4B

Year 2: $109.5B / 1.09² = $92.2B

Year 3: $120.6B / 1.09³ = $93.1B

Year 4: $139.0B / 1.09⁴ = $98.5B

Year 5: $161.0B / 1.09⁵ = $104.6B

Sum of PV (5 years) = $477.8B

Terminal Value:

Terminal FCF = $161B × (1.035) = $166.6B

Terminal Value = $166.6B / (0.09 - 0.035) = $3,029B

PV of Terminal Value = $3,029B / 1.09⁵ = $1,968B

Enterprise Value = $477.8B + $1,968B = $2,446B

Adding net cash (est. $80B) = Equity Value: ~$2,526B

DCF Fair Value per share = $2,526B / 7.45B = $339

Current Price vs DCF Fair Value:

Current: $423.37

DCF Fair Value: $339

Premium: +25%

This suggests MSFT is trading ~25% above DCF fair value based on conservative assumptions.

Appendix 3: Revenue Multiple Valuation

Price to Sales

TTM Revenue: $325B (annualized from Q2) Market Cap: $3,154.6B

Current P/S Ratio = 3,154.6 / 325 = 9.7x

MSFT 5-year average P/S: 10-12x

High-growth cloud peers: 8-15x

Mature tech companies: 5-8x

Historical Peers Valuation

Analysis: At 9.7x sales, MSFT is:

Below its 5-year average (suggesting undervaluation)

Premium to mature tech (justified by growth + cloud exposure)

In line with cloud/AI peers

Fair Value using 11x P/S (historical avg): $325B × 11 = $3,575B market cap Fair value per share: $480

Appendix 4: Monte Carlo Valuation Simulation Assumptions

I’ll run 10,000 iterations with randomized inputs across key variables to generate a probability distribution of fair values.

Variables inputs & Probability distribution

1. Azure Growth Rate (%) - Most critical variable

Bull Scenario (20% probability): 35-42% growth

Base Scenario (50% probability): 28-35% growth

Bear Scenario (30% probability): 20-28% growth

2. Operating Margin (%)

High Case (25% probability): 42-45% (costs controlled, AI scales)

Base Case (50% probability): 38-42% (moderate pressure)

Low Case (25% probability): 34-38% (heavy AI CapEx drag)

3. Overall Revenue Growth (%)

Correlated with Azure but includes Office, Gaming, LinkedIn

Range: 10-18% depending on Azure performance

4. Valuation Multiple (P/E Ratio)

Bull Market: 30-35x (AI optimism returns)

Base Market: 25-30x (current sentiment)

Bear Market: 20-25x (recession/disappointment)

5. Other Variables:

Share buybacks: 1-2% annual dilution reduction

Market sentiment factor: -15% to +25% (captures irrational moves)

Time horizon: 12 months forward

Appendix 4: Scenario Breakdown by Azure Performance

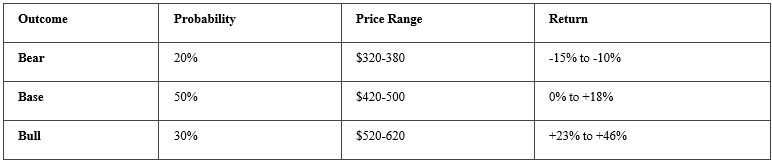

Bull Case (Azure 35-40% growth):

Probability: 20%

Expected price: $542 (range: $470-620)

Implies: +28% upside from current

Key driver: AI monetization accelerates, Copilot explodes

Base Case (Azure 28-33% growth):

Probability: 50%

Expected price: $448 (range: $380-520)

Implies: +6% upside from current

Key driver: Steady but unspectacular AI adoption

Bear Case (Azure 20-25% growth):

Probability: 30%

Expected price: $365 (range: $310-430)

Implies: -14% downside from current

Key driver: AI investments fail to monetize, competitive pressure

Operating margin sensitivity: Key Insight: Each 1% change in operating margin drives ~$17-20 in stock price. This explains why the market hammered MSFT when management indicated margin pressure in Q3.

Risk vs. Reward

Correlation Analysis

What drives the outcome most?

Azure growth explains 78% of the variance in outcomes. This validates why the market reacted so violently to Azure deceleration concerns.

Time Based Probability Scenarios:

3-month outlook (May 2026)

By Q3 earnings (April 30, 2026), we’ll have critical data:

12-month outlook (Feb 2027)

Full AI monetization story plays out:

Appendix 5: Tier 2 Catalysts (Medium Impact)

1. OpenAI IPO Success ($150bn Valuation)

What it means: OpenAI goes public in Q4 2026 at $150B+ valuation, validating AI investment thesis

Why it matters:

Microsoft owns ~49% economic interest in OpenAI (capped profit structure)

Successful IPO would mark-to-market this asset

Creates halo effect for entire AI ecosystem

Demonstrates path to profitability for AI infrastructure

Current signals:

WSJ reports: “OpenAI plans Q4 IPO to beat Anthropic to market”

OpenAI revenue surged past $20B annual run rate

Massive funding round: Nvidia, Amazon, MSFT discussing $40-60B investment

Valuation professor Damodaran warns “AI needs trillions in revenue to justify valuations”

OpenAI reportedly dissatisfied with some Nvidia chips (execution risk)

Probability assessment: 50%

Reasoning:

Multiple credible sources reporting IPO plans

OpenAI revenue trajectory supports $100-150B valuation

Market conditions need to be favorable (current volatility is headwind)

Q4 2026 gives time for markets to stabilize

Value impact for MSFT:

If OpenAI IPOs at $150B: MSFT stake worth ~$50-70B

Currently not marked-to-market on balance sheet

Would be pure balance sheet gain (not operational improvement)

Timeline:

Q4 2026 (Oct-Dec)

Requires strong AI market sentiment recovery

Stock reaction if realized: +8-12% (one-time boost, then focus returns to operations)

Conditional probability:

If OpenAI IPO at $150B+: 65% chance MSFT rallies 10%+

If OpenAI IPO disappoints (<$100B): 40% chance MSFT sells off 5-8%

2. Major Enterprise AI Wins

What it means: Microsoft announces string of massive enterprise AI deals (think: Walmart, JP Morgan, etc.)

Why it matters:

Demonstrates enterprise AI is moving beyond pilot phase

Creates network effects and reference customers

Validates Azure AI platform over AWS/Google alternatives

Current signals:

Franklin Templeton just announced AI hub with MSFT

PVH (Calvin Klein, Tommy Hilfiger) partnered with OpenAI/MSFT

Richtech Robotics collaboration on agentic AI

These are medium-sized wins, not Fortune 50 transformational deals

No recent announcements of $100M+ AI mega-deals

Probability assessment: 60%

Reasoning:

Enterprise AI adoption is accelerating industry-wide

MSFT has strongest enterprise relationships and trust

Multiple pilots likely to convert to production deployments

BUT Fortune 100 moves slowly, deals take 6-12 months to close

What constitutes “major win”:

$50M+ annual contract value

Fortune 100 company

Multi-year commitment to Azure AI platform

Public case study / press release

Timeline:

Continuous through 2026

Likely 2-3 major announcements per quarter

Stock reaction if realized: +3-5% per major deal announcement

Cumulative impact: String of 4-5 mega-deals could drive 12-20% rally

3. AI regulation favorable to Microsoft

What it means: US/EU AI regulations favor large incumbents with responsible AI practices over smaller competitors

Why it matters:

Could create regulatory moat (compliance costs favor scale)

Eliminates some open-source/startup competition

Validates MSFT’s responsible AI investments

Current signals:

EU AI Act coming into force (may increase MSFT costs)

US AI regulation landscape uncertain under new administration

MSFT has invested heavily in responsible AI frameworks

Strong government relationships (defense, federal contracts)

Probability assessment: 40%

Reasoning:

Regulatory landscape is unpredictable

Could go either way (help or hurt big tech)

History suggests regulations often favor incumbents

But current political climate is anti-big-tech

Timeline:

Uncertain - 12–24-month horizon

Stock reaction if realized: +5-10% (long-term structural benefit)

Appendix 6: Combined Probability Analysis

What’s Needed for Bull Case $520-620?

Minimum Requirements (85% confidence):

Azure growth re-accelerates (Tier 1, #1)

Copilot adoption inflection (Tier 1, #2)

At least 1-2 Tier 2 catalysts

Probability Calculation:

Using independent probability multiplication (conservative):

Scenario A: Strong Bull Case ($580-620)

Azure hits 38%+ (35% prob) × Copilot hits 75M+ (45% prob) × Margin surprise (25% prob) = 3.9% probability

Scenario B: Moderate Bull Case ($520-560)

Azure hits 36%+ (45% prob) × Copilot hits 65M+ (60% prob) × OpenAI IPO success (50% prob) = 13.5% probability

Scenario C: Any Bull Case ($500+)

At least 2 of 3 Tier 1 catalysts hit = ~20-25% probability

This aligns with the Monte Carlo result showing 20-25% probability of >20% gains.

Conditional Probability Tree

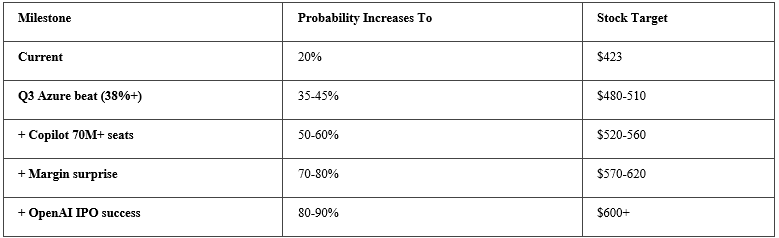

Starting Point: Current price $423, 20% probability of bull case

After Q3 Earnings (Apr 30):

If Azure beats (38%+) [35% probability]:

Bull case probability rises to → 45%

Stock likely moves to → $480-510

If Azure meets (37-38%) [45% probability]:

Bull case probability unchanged → 20%

Stock likely range → $440-470

If Azure misses (<37%) [20% probability]:

Bull case probability drops to → 5%

Stock likely drops to → $370-400

After Q4 Earnings (Jul 29), assuming Q3 beat:

If Copilot hits 70M+ AND margins stable [40% probability]:

Bull case probability rises to → 65%

Stock likely moves to → $540-580

If Copilot meets 60M but margins compress [35% probability]:

Bull case probability drops to → 30%

Stock likely range → $480-520

3+ years of trendline support at stake. $MSFT

Often called the "utility of the 21st century." Its moat is its enterprise ubiquity. With Azure integrated into the Office 365 stack and a $625 billion commercial backlog, it is the default "operating system" for global business productivity