Intel Corp. (INTC) Executive Summary: Can Intel Truly Catch TSMC, or Is 18A Too Little, Too Late?

Despite major partnerships, manufacturing credibility took a hit following the Nvidia testing halt. Competing against TSMC with a decade-long head start means the margin for error is thin.

Company Overview

Intel Corporation, headquartered in Santa Clara, California, is a global leader in designing, developing, and manufacturing cutting-edge computing and related products. Established in 1968, the company operates through three main segments: Intel Products, Intel Foundry, and All Other.

Intel’s diverse product portfolio includes microprocessors, chipsets, standalone system-on-chip (SoC) solutions, and multichip packages, alongside hardware products such as CPUs, GPUs, accelerators, and field-programmable gate arrays (FPGAs).

Additionally, Intel provides memory, storage, connectivity, and networking solutions, catering to a wide range of industries and applications.

The company also offers optimization solutions for various workloads, such as AI, security, and networking, and delivers intelligent edge platforms for enhanced automation and data integrity.

The company is serving a broad customer base, including original equipment manufacturers, cloud service providers, and other manufacturers.

Price Action & Technical Context

Current price: $39.37 (as of Jan 5, 2026)

The price action shows a brutal multi-year decline bottoming around $18.13 in April 2025, followed by a strong recovery rally. Key observations from your chart:

The $24-25 range (Sept 2025) marked a critical inflection point where INTC broke out

A powerful surge in September 2025 took price from ~$25 to $42+ in weeks

Since peaking near $43.76 (Dec 3, 2025), we’re seeing consolidation with higher lows being maintained

The 50-day SMA on your chart is around $28-30, price is well above it, confirming intermediate-term uptrend

VWAP anchored to 80-period low sits around $32, price holding above suggests buyers in control from that major bottom

Fundamentals & Earnings

The fundamentals tell a turnaround story with execution risk:

Recent earnings:

Q3 2025: $0.23 EPS (vs -$0.04 est), massive beat, +675% surprise

Revenue: $13.7B (+2.78% YoY, beat by 4%)

Q2 2025: -$0.10 EPS miss, still losing money

2024 was brutal: Q3 2024 posted -$0.46 EPS

Revenue is essentially flat (~$12.7-14.3B range), while profitability swings wildly. Intel is not growing, they’re restructuring.

Catalysts & News

Bullish developments:

Nvidia invested $5 billion (Sept 2025), 214.8M shares at $23.28. This is validation of Intel’s foundry strategy

SoftBank deal announced for foundry business

18A process technology launched at CES 2026 (Jan 5), “Panther Lake” chips shipping, CEO claims “over-delivered” on timeline

New CEO Lip-Bu Tan (semiconductor industry veteran) driving aggressive turnaround

Stock up 79% in 2025 per recent reports

Bearish concerns:

Nvidia reportedly halted testing of Intel’s 18A process (Dec 24), significant setback for foundry credibility

Removed from Dow Jones in Nov 2024, replaced by NVDA

Dividend slashed from $0.365 to $0.125 (2023) and hasn’t increased since

Two analyst downgrades to “sell” in Oct (HSBC, Bank of America)

Manufacturing execution remains unproven vs TSM

Analyst & Institutional Sentiment

Mixed but improving:

Recent upgrade: Melius Research to Buy ($50 target, Jan 5, 2026)

Most analysts at “Hold”, 15+ price target raises in Q4 2025

Price targets range: $25-52, consensus gravitating toward $35-40

Congress members buying heavily (Rep. Tim Moore made multiple purchases Jul-Aug 2025)

Insider selling is minimal and appears routine

Bottom Line

Intel finds itself at a critical crossroads, operating as a high-risk turnaround. While the stock has staged a remarkable rally of over +85% from its April 2025 lows fueled by strategic investments from the likes of Nvidia and SoftBank, the fundamentals tell a more complex story. The company is aggressively executing under new leadership and has reached a pivotal milestone with its 18A process nodes shipping, yet it continues to struggle with stagnant revenue growth and inconsistent profitability.

The primary hurdle remains Intel’s ambition to challenge TSMC in the foundry space. Despite major partnerships validating the current strategy, manufacturing credibility took a visible hit following the Nvidia testing halt. Competing against a dominant incumbent with a decade-long head start means the margin for error is thin.

From a technical perspective, the stock is currently in a consolidation phase following its massive run. Price action is testing the $36–$40 range to determine if a sustainable new base can be established. If this level holds, the next leg higher could target the $45–$50 zone. However, should this support crumble, investors should brace for a retracement to the $32–$34 level.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. All opinions expressed are my personal views. Always do your own research and consult with qualified professionals before making investment decisions.

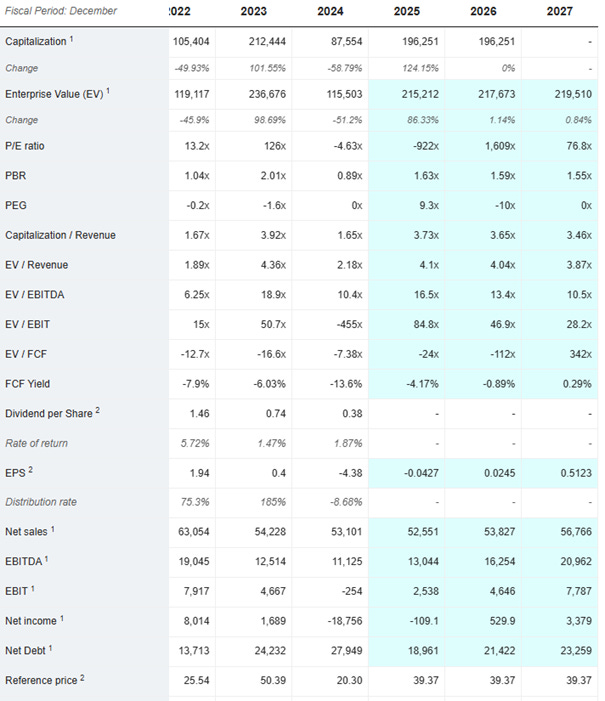

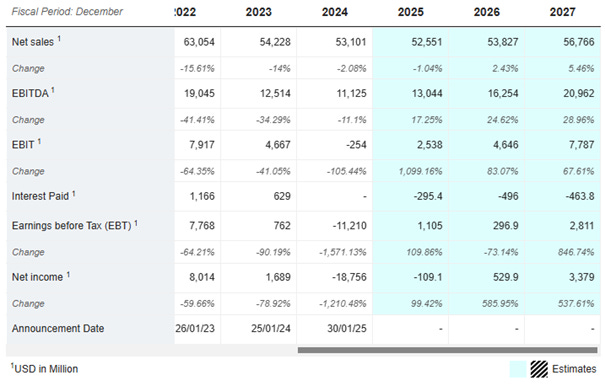

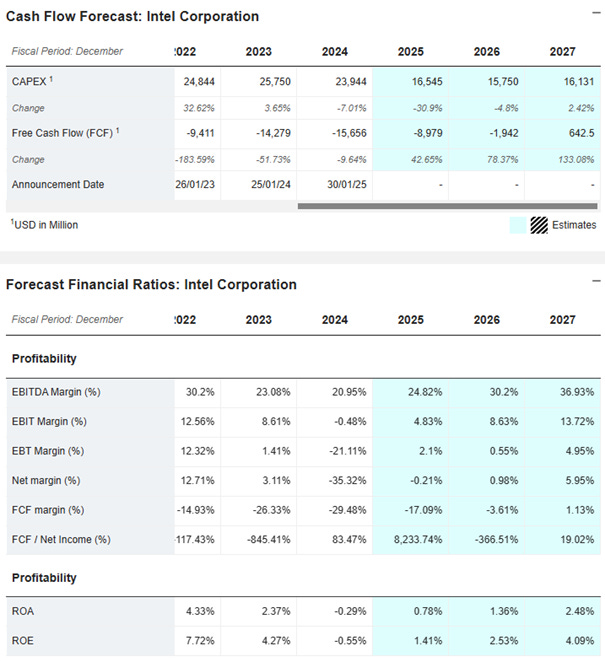

Appendix 1: Financial Projections

Appendix 2: Valuation Metrics