Marvell Technology (MRVL) Executive Summary: Is Marvell at $87 is a Christmas Gift?

Data center revenue is now 72%, fueled by a custom ASIC business with titans like Amazon and Microsoft and a strategic $3.25B bet on Celestial AI for next-gen photonics.

Company Overview

Marvell Technology is a provider of data infrastructure solutions that span from the data center core to the network edge. The company is headquartered in Wilmington, Delaware, and operates in several global markets. Established in 1995, Marvell specializes in developing complex System-on-a-Chip architectures that integrate analog, mixed-signal, and digital signal processing functionalities.

Marvell’s product portfolio includes Ethernet solutions, custom application-specific integrated circuits (ASICs), storage controllers, and interconnect products like pulse amplitude modulation (PAM) digital signal processors (DSPs). These products are essential for data centers, enterprise networking, carrier infrastructure, consumer electronics, and automotive/industrial markets. The company notably serves the burgeoning data center market, supporting cloud and AI systems with innovative technologies such as silicon photonics and co-packaged optics.

Marvell has strategically positioned itself as a key player in the AI and data center sectors by acquiring companies like Celestial AI, which enhances its capabilities in optical interconnects. The company’s solutions are highly integrated and tailored to individual customer needs, leveraging over 10,000 patents. As a fabless company, Marvell outsources the fabrication of its semiconductors to focus on design and marketing, ensuring flexibility and cost efficiency.

Marvell Technology develops the networking, custom silicon, and interconnection that allow AI systems to scale efficiently. As AI models grow larger and more distributed, data movement becomes a critical bottleneck, placing MRVL at the heart of the data center architecture.

The AI Infrastructure Story

Data center revenue now represents 72% of total revenue (up from 40% in FY2024)

Custom ASIC business with hyperscalers (Amazon, Microsoft) ramping to $2B by 2028

Recent $3.25B acquisition of Celestial AI (photonics) positions them for next-gen AI connectivity

Management expects data center revenue to grow >25% in FY2027

Price Action & Technical Context

MRVL closed at $87.68 on Dec 23, showing strength after recovering from recent volatility. The stock has been in a volatile trading range:

Recent High: $102.77 (Dec 3, 2025)

Recent Low: $47.31 (Apr 4, 2025)

YTD Performance: Down significantly from highs above $125 in Jan 2025

The daily chart shows significant choppiness with the stock experiencing a sharp decline from March-April tariff-related selloff, followed by a strong recovery into late November/early December on earnings optimism, then another pullback

Fundamentals

Earnings Momentum is Explosive:

Q3 FY2026 (Dec 2): Beat estimates with $0.76 EPS vs $0.67 est, revenue $2.08B

Massive YoY Growth: EPS up 77%, Revenue up 37%

Last 4 quarters show consistent EPS growth: 5% → 123% → 158% → 77% YoY

Company guiding for $10B revenue next year (25% data center growth)

Analyst Sentiment: Mixed but Improving

Recent Activity (Post-Earnings):

Massive price target raises post-Dec earnings: Targets now range $90-$156

Benchmark downgraded to Hold on Dec 8 (citing Microsoft/Amazon concerns)

Bank of America downgraded to Neutral on Aug 29 (growth pace concerns)

But multiple upgrades in Dec: Oppenheimer to $150, Evercore to $156, Wells Fargo to $135

The Bear Case: Near-term customer program uncertainties, potential delays in hyperscaler deployments, valuation concerns after the rally

The Bull Case: Long runway for AI infrastructure buildout, custom silicon wins, strong competitive position in optical DSPs and networking

Corporate Developments

$5B Share Buyback Program announced Sept 24 (nearly 10% of market cap)

Celestial AI Acquisition for $3.25B, photonics technology for AI data centers

Sold Auto Unit for $2.5B to focus entirely on data center business

Insider Activity: Executives (including CEO) bought shares in Sept at $77-78 range

Risks Involved

Customer Concentration: One hyperscaler customer represents significant revenue

Competition: Broadcom dominates custom AI chip market; concerns about MRVL potentially losing Microsoft business to Broadcom

Tariff/Trade Risks: Stock highly sensitive to US-China trade tensions

Q3 Guidance Miss: While Q3 beat, Q4 guidance midpoint ($2.2B) slightly below estimates triggered selloff

Bottom Line

Marvell is undergoing a fundamental business transformation, pivoting into the heart of AI data center infrastructure. The “inflection point” for revenue and earnings is no longer a projection, it is an accelerating reality. Management has demonstrated execution in their custom silicon strategy, positioning the firm as a primary beneficiary of the AI build-out. This operational success, coupled with a balance sheet recently fortified by strategic asset sales, paints a picture of a company hitting its stride at the perfect technological moment.

However, Marvell remains a “high-beta” play, frequently caught in the crosshairs of macro volatility and tariff-related headlines. While the long-term AI story is intact, near-term visibility is clouded by the unpredictable deployment schedules of major hyperscalers. The competitive landscape is heating up; Marvell is locked in an intense battle with Broadcom for custom chip dominance

At current levels, $87 per share the valuation feels significantly more grounded than the triple-digit peaks seen in December. While the fundamental story of explosive revenue growth and margin expansion is compelling, the stock’s tendency to “get ahead of itself” suggests that timing and entry points are everything.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. All opinions expressed are my personal views. Always do your own research and consult with qualified professionals before making investment decisions.

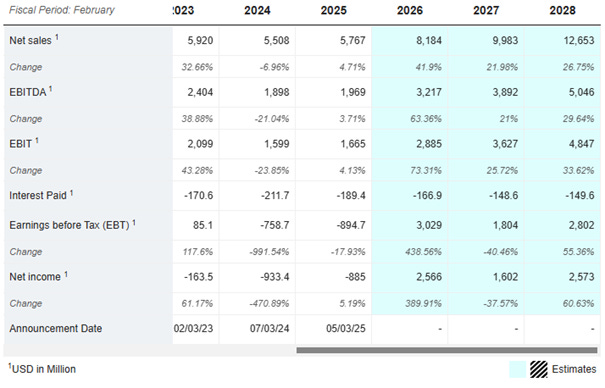

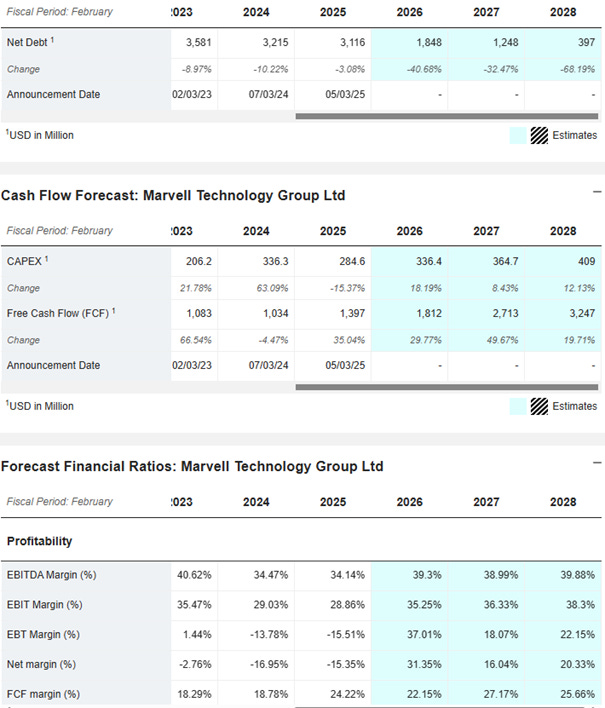

Appendix 1: Financial Projections

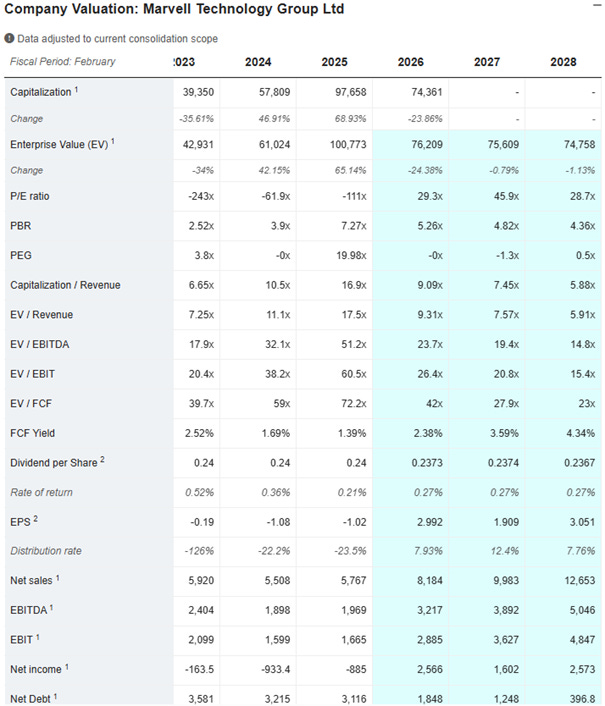

Appendix 2: Valuation Metrics

One additional layer worth calling out is how photonics and materials constraints reinforce this thesis.

As AI data centers scale, the challenge isn’t just compute, it’s the physical limits of moving data. Traditional copper interconnects are running into bandwidth, latency, and power-efficiency ceilings at scale. That’s where photonics becomes critical.

Companies like LITE (Lumentum) and photonics innovators play an important role in enabling higher-bandwidth, lower-latency optical interconnects that can keep pace with massive AI model growth. At the same time, companies building optical DSPs, co-packaged optics, and photonic interconnects are helping solve the bottleneck between chips, racks, and data center fabrics.

This isn’t just about faster chips, it’s about enabling the entire infrastructure layer to scale. The interplay between advanced silicon, optical connectivity, and materials engineering is a major structural driver of the AI build-out.