Meta Platforms (META) Executive Summary: Why Flawless Earnings Aren’t Saving Meta

9 Consecutive Beats and a 25% drop, is this the greatest buying opportunity of 2026?

Company Overview

Meta Platforms, formerly known as Facebook is a prominent technology company headquartered in Menlo Park, California. It operates through two main segments: Family of Apps (FoA) and Reality Labs (RL).

The FoA segment includes platforms like Facebook, Instagram, Messenger, WhatsApp, and Threads, which facilitate social interaction and communication. These platforms generate revenue primarily through advertising, connecting marketers with a wide audience across their applications.

The RL segment focuses on virtual and augmented reality products, such as Meta Quest devices and AI glasses like Ray-Ban Meta and Oakley Meta glasses, aimed at creating immersive social experiences.

Meta is heavily invested in AI, integrating advanced AI models across its platforms to enhance user engagement and advertising efficiency.

Founded in 2004, Meta has evolved beyond traditional social media, pursuing innovations in virtual reality and AI to establish a new computing platform. The company collaborates with industry leaders like Microsoft, NVIDIA, and AMD to advance its technological capabilities. Meta’s strategic focus includes expanding its AI infrastructure, enhancing its product offerings, and maintaining its competitive edge in the digital advertising market.

Meta’s unique value proposition lies in its vast user base and its integration of AI into its social platforms, enhancing user engagement and ad targeting. The company’s investment in AI and its focus on building a personal superintelligence differentiate it in the tech landscape. Meta’s ability to leverage its extensive network of apps and its development of new technologies in virtual reality and AI positions it as a leader in creating immersive and personalized digital experiences.

Recent Developments

The AI Transformation: Meta is doubling down on its technical backbone through a massive $12 billion deal with Nebius to secure AI cloud infrastructure, specifically leveraging the NVIDIA Vera Rubin platform. This move is being paired with the internal development of custom silicon through their MTIA chips as they roll out Meta AI support on a global scale. However, this aggressive expansion comes with a steep human cost, as the company is considering potential 20% workforce layoffs to fund these heavy AI capital expenditures, a move that has resulted in mixed reactions from the market.

Product Setbacks and Internal Shifts: The road to AI dominance hasn’t been entirely smooth, as the company’s “Avocado” model has reportedly been delayed after failing to meet performance benchmarks against competitors like Google and Anthropic, causing a noticeable dip in the stock price. We are also seeing a significant metaverse pullback, with Meta discontinuing a key VR product to narrow its focus. Interestingly, Mark Zuckerberg is reportedly building a personal AI agent to assist with his CEO duties, signaling his deep personal commitment to the technology.

Legal and Geopolitical Headwinds: On the legal front, the company is facing substantial pressure. A jury recently deadlocked in a high-profile social media addiction trial, and Meta was hit with a $375 million verdict in a New Mexico child exploitation case. Adding to these domestic issues is a layer of geopolitical risk, as Chinese regulators have placed Meta’s approximately $2 billion acquisition of Manus under intense scrutiny.

Price Action & Technical Context

Looking at the recent price action, the stock has been on a significant journey over the last year and a half. It went on an absolute tear starting from its 2024 lows, eventually reaching a peak of approximately $796 in August 2025. Since hitting that high, however, the performance has shifted into a -25.5% drawdown, bringing the price to its current level of around $593.

We saw a major moment of volatility back in April 2025 when a tariff panic caused a flush in the price, dropping it down to approximately $479. While the stock managed to bounce hard off those lows, it has yet to reclaim its former momentum. Currently, the price is sitting in a middle-ground at about $593, where it has spent the past few weeks grinding sideways as the market decides on its next major move.

Business Performance

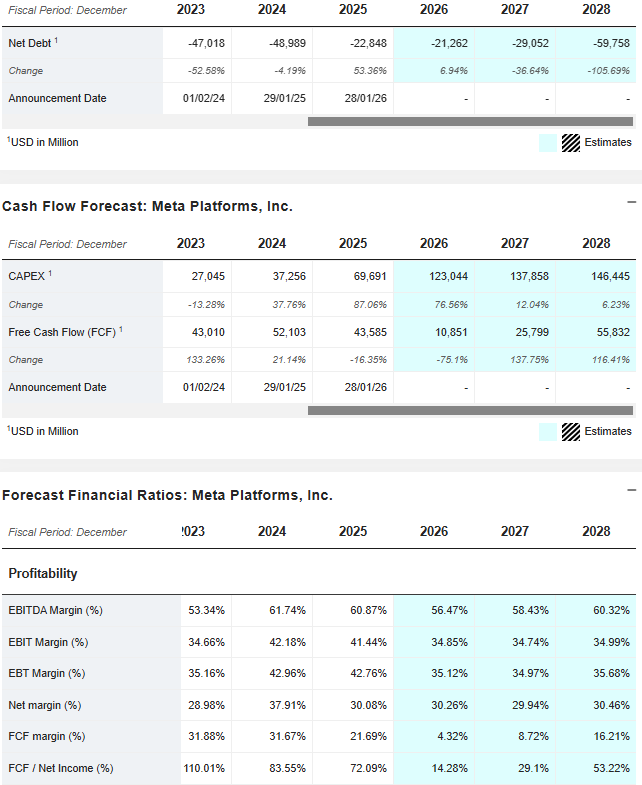

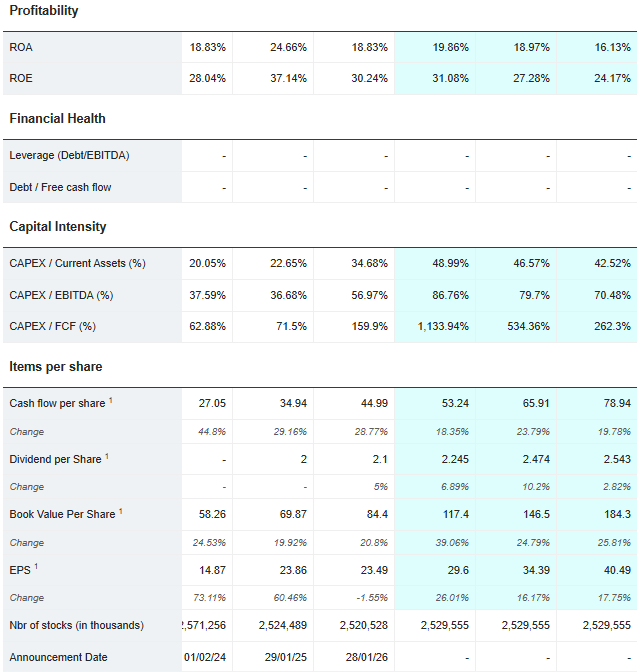

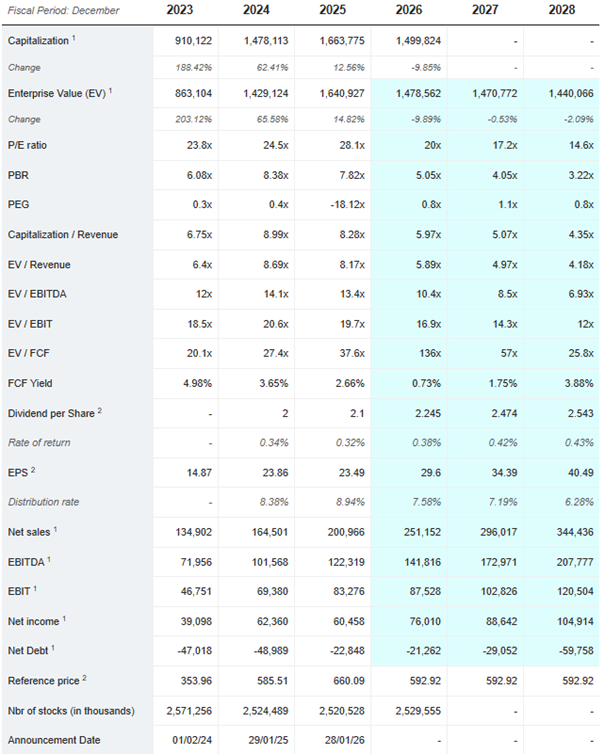

When we look at the underlying fundamentals, this business remains outstanding. For a company growing its earnings per share by more than 30% YoY, a PE ratio of 28x is arguably not even stretched, especially when you consider the current growth trajectory. The profitability metrics are equally impressive, as the company is maintaining gross margins of approximately 82% and net margins of around 38%.

Looking closer at the Q4 2025 data, the company’s valuation sits at a trailing P/E of 28.4x and P/S ratio of 8.8x. Its EV/EBITDA ratio currently stands at 16.6x, which supports the argument that the valuation is reasonable relative to its scale. Perhaps most importantly for investors, the free cash flow is absolutely gushing, with $13.0 billion generated in the last quarter alone. With a total market capitalization of approximately $1.53 trillion, fundamentals suggest a very strong financial position despite the recent market volatility.

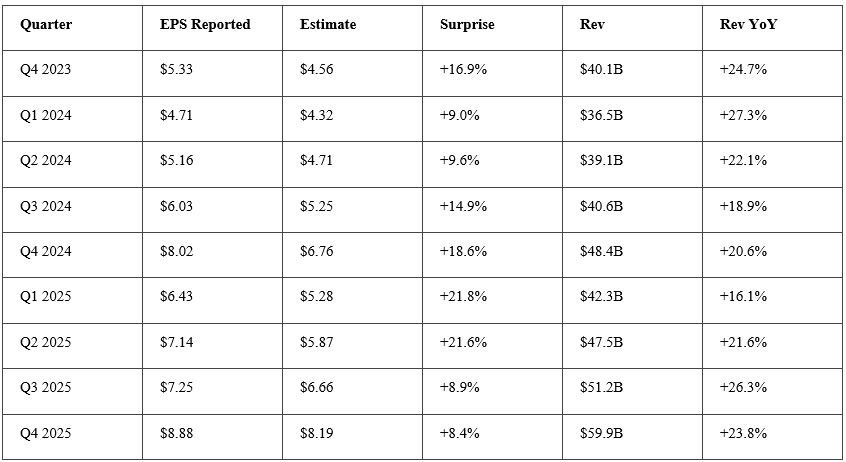

It is remarkable to see a track record of nine consecutive earnings beats without a single miss. This consistent outperformance is impressive when you consider that revenue is actually accelerating, reaching a massive $59.9B in Q4 2025 alone. Under normal market conditions, you would expect this level of fundamental strength to drive the stock price significantly higher. However, as we have seen with the recent sideways movement and the -25.5% drawdown from the peak, the market is currently weighing the financial results against the broader legal risks and the heavy capital spending required for the AI push.

Analyst Sentiment

The sentiment across the analyst community remains bullish, with more than 30 buy ratings from major financial houses issued in 2026 alone. There are currently barely any hold ratings on the stock and zero sell ratings. The price targets currently range from a low end of $700 to an optimistic high of $1,144 from Rosenblatt. On average, the Wall Street consensus sits at roughly $850, a target that implies approximately 43% upside from the current price of around $593.

Insider Activity & Congress Trading

When examining recent insider activity, we see almost exclusively selling across the board, though it is important to note that these are all pre-planned and scheduled transactions. Key executives including COO Olivan, CLO Newstead, CFO Li, and CTO Bosworth have been offloading shares, but this appears to be routine behavior. We did see notably heavier selling from CFO Susan Li during the February and March 2026 period, totaling in the $83M range, but even this remains within the expected scope of normal compensation liquidation for an executive at this level.

On the legislative side, there have been some small-scale purchases by a handful of Democratic and Republican members of Congress, specifically Representatives Fields, Cisneros, and McCaul, between January and February 2026. These buys were mostly in the $1K to $250K range, and interestingly, most of these positions are currently underwater given the stock’s recent performance. Ultimately, there is nothing dramatic to report here, as the activity suggests standard portfolio adjustments rather than a major shift in conviction.

Bottom Line

The business is currently firing on all cylinders, with revenue, earnings per share, and margins all reaching exceptional levels. This fundamental strength is bolstered by an aggressive and credible AI investment strategy that has earned the overwhelming approval of Wall Street analysts. Despite the rapid expansion, the P/S ratio remains reasonable when measured against the company’s current growth rate. From a price action perspective, the stock showed significant resilience by holding the $479 low in April and subsequently recovering approximately 24% from that level.

However, significant risks remain as the stock has retreated roughly 25% from its all-time highs despite delivering flawless earnings reports. The broader market is facing macro headwinds, including oil at $110, persistent stagflation fears, and a repricing of interest rate expectations that continue to pressure the entire tech sector. Internal challenges such as the delay of the “Avocado” AI model suggest increasing competitive pressure from Google and Anthropic, while ballooning capital expenditures raise uncertainty regarding long-term returns on investment. These issues are compounded by a heavy legal overhang involving addiction trials and child safety, alongside geopolitical friction surrounding the Manus acquisition in China and internal efficiency pressures signaled by recent layoffs.

Technically, the stock is currently hovering between $590 and $595, a zone that served as a critical support level in late 2024. For a true recovery to take shape, the price needs to hold this immediate area and successfully reclaim the $630 to $640 range. If macroeconomic conditions continue to worsen and this support fails to hold, the $479 low from April remains the most important downside reference point for investors to monitor.

***

Disclaimer: This content is for informational purposes only and does not constitute financial advice. All opinions expressed are my personal views. Always do your own research and consult with qualified professionals before making investment decisions.

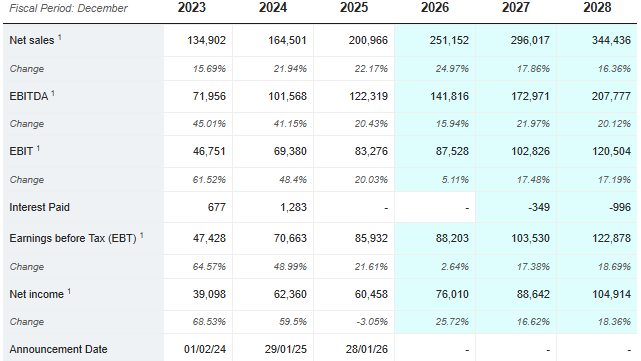

Appendix 1: Financial Projections

Appendix 2: Valuation Metrics

Significant risks remain: Internal challenges such as the delay of the "Avocado" AI model suggest increasing competitive pressure from Google and Anthropic, while ballooning CAPEX raise uncertainty regarding long-term ROI. These issues are compounded by a heavy legal overhang involving addiction trials and child safety, alongside geopolitical friction surrounding the Manus acquisition in China and internal efficiency pressures signaled by recent layoffs.