Micron Technology (MU) Executive Summary: Is the AI Supercycle Over? What Micron's Volatility Really Tells You About the AI Trade

Only U.S.-based memory manufacturer with growth driven by AI/ high-bandwidth memory demand. Analyst upgrades accelerating into year-end but valuation is stretched after massive rally.

Company Overview

Micron Technology is a leading provider of memory and storage solutions, with a focus on transforming how information is used worldwide. The company operates across the United States, Taiwan, Singapore, Japan, Malaysia, China, and India. Micron’s business is structured into four primary units: Cloud Memory Business Unit (CMBU), Core Data Center Business Unit (CDBU), Mobile and Client Business Unit (MCBU), and Automotive and Embedded Business Unit (AEBU). These units cater to the data center, PC, graphics, networking, automotive, industrial, and consumer embedded markets.

The company generates significant revenue from its dynamic random-access memory (DRAM) products, which are crucial for data retrieval in various applications, including data centers and mobile devices. Micron also leads in high-bandwidth memory (HBM) and NAND flash memory, serving applications that require high data throughput, such as AI and high-performance computing. Its product portfolio includes advanced solutions like 1γ DRAM and G9 NAND technologies.

Micron is undoubtedly riding the AI memory supercycle, and the long-term fundamentals around HBM and next-gen tech leadership are robust. However, investors must recognize that the stock has already priced in a significant amount of good news.

Price Action and Technical Picture

MU closed at $237.22 on Dec 5, 2025

Recent volatility: The stock experienced a sharp selloff from ~$260 (Nov 17) down to ~$192 (Nov 20), a brutal -26% drop in 3 days

Strong recovery: Since the Nov 20 low, the stock has rallied +23% back to current levels

6-month range: $104-$260, showing extreme volatility through the year

YTD performance: Up approximately 119% from ~$108 in early August to current levels

The daily: The stock is back above key support at $230, but faces resistance around $250-$260 from the mid-November highs. The recovery from $192 has been impressive, but watch for consolidation or another test of support if broader tech weakness returns.

Strategic Positioning

Technology Leadership:

Only U.S.-based memory manufacturer - geopolitical advantage

First to ship 1γ DRAM with EUV

HBM3E leadership with HBM4 on track for 2026

G9 NAND in volume production

Capital Investments:

Massive fab expansion in U.S. (CHIPS Act support)

Building new facilities in New York and other locations

Partnerships with TSMC for HBM4E base logic die manufacturing

AI Tailwind:

CEO states “AI is the driver of our growth”

Each AI server requires 8-12x more DRAM than traditional servers

HBM content growth driving ASP expansion

Micron is sole U.S. HBM supplier to Nvidia’s AI platforms

Financial Performance: Spectacular turnaround

Earnings Progression (Quarterly EPS):

Q2 2024: $0.42

Q3 2024: $0.62

Q4 2024: $1.18

Q1 2025: $1.79 (+288% YoY)

Q2 2025: $1.56 (+271% YoY)

Q3 2025: $1.91 (+208% YoY)

Q4 2025: $3.03 (+157% YoY) - Beat estimates by 8.6%

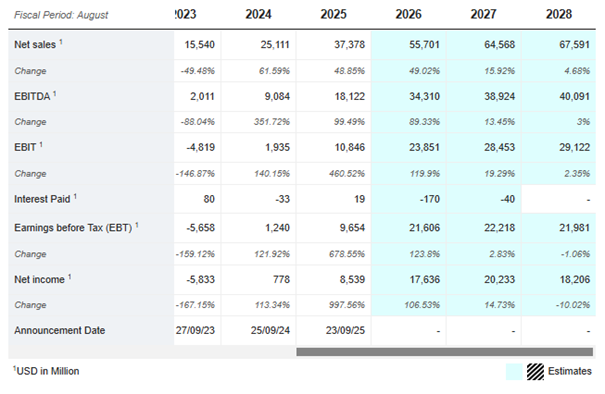

Revenue Growth:

Q4 2025: $11.3B (+46% YoY) - Beat estimates by 1.35%

FY2025 total: $37.1B (~84% increase YoY)

DRAM revenue: $28.6B (77% of total)

NAND revenue: $8.5B (23% of total)

Guidance Update (Aug 11, 2025): Micron raised Q4 guidance mid-quarter citing improved pricing (especially DRAM) and strong execution, which triggered a rally in the stock.

Analyst Sentiment: Overwhelmingly Bullish

Morgan Stanley: Upgraded to Overweight, PT $338 (Nov 24)

Wells Fargo: PT $300

UBS: PT $275

JP Morgan: PT $220

Citigroup: PT $275

Mizuho: PT $270

Rosenblatt: PT $300

Consensus: 29 analysts covering the stock, with the vast majority maintaining “Buy” or “Overweight” ratings. Only a few holdouts (Goldman Sachs at Neutral $205, Morgan Stanley previously at Hold).

The recent upgrade wave in September-November 2025 following strong Q4 earnings shows analysts are becoming more confident in the AI-driven memory supercycle.

Business Unit Performance

Cloud Memory (CMBU) - The Star Performer:

Revenue: $13.52B in 2025 (vs. $3.79B in 2024) - +257%

HBM dominance: Shipping HBM3E 12-high as majority of HBM shipments

HBM4 sampling: 36GB 12-high samples delivered to key customers for next-gen AI platforms

Leading-edge 1γ (1-gamma) DRAM node with EUV lithography in production

This segment is driving the massive growth story

Core Data Center (CDBU):

Revenue: $7.23B (up from $4.98B)

Strong DDR5 adoption in servers

Data center SSD portfolio (9550, 6550 ION series) with G8 and G9 NAND

Mobile & Client (MCBU):

Revenue: $11.86B (relatively flat YoY)

LPDDR5X for flagship smartphones with 1γ node

Client SSDs benefiting from AI PC adoption

Automotive & Embedded (AEBU):

Revenue: $4.75B (modest growth)

Automotive LPDDR5X in production

First automotive-qualified enterprise SSD (4150)

Key Risks and Headwinds

China Situation:

May 2023 CAC decision banning Micron products from critical infrastructure continues to impact

October 2025: Micron exiting China’s data center market following the ban

Lost significant market share (~95% to 0% in certain segments per Jensen Huang comments about Nvidia)

Competitive Landscape:

Samsung, SK Hynix remain formidable competitors

Chinese competitors (CXMT, YMTC) receiving government subsidies

Risk of oversupply if competitors ramp aggressively

Recent Volatility Triggers:

Nov 20 selloff driven by sector-wide concerns about AI valuations

Trade tensions and tariff risks (Trump administration chip tariff threats)

Supply chain constraints for rare earth materials

Valuation Concerns:

Stock has more than doubled YTD

Trading at elevated multiples relative to historical norms

Options market shows heavy activity, suggesting speculative positioning

Insider & Institutional Activity

Insider Selling:

CEO Sanjay Mehrotra has been selling regularly (mostly scheduled sales)

EVP Scott DeBoer sold $18.3M in late October

CFO Mark Murphy sold $28.4M in late October

This appears to be part of regular executive compensation liquidation, not necessarily bearish signals

Government/Political Trading:

Rep. Ro Khanna (D) has been very active - both buying and selling

Recent activity shows profit-taking after strong run

Institutional (13F):

Hedge funds increased positions in Q2/Q3 (David Tepper’s Appaloosa doubled stake to 825K shares)

Micron is a top holding for many tech-focused funds

Recent News Highlights

Dec 3: Micron exits Crucial consumer business to focus on enterprise/AI (strategic refocusing)

Nov 24: Morgan Stanley upgrade to $338 PT

Nov 13: Shipped automotive UFS 4.1 samples (4.2 Gb/s bandwidth)

Oct 22: Announced 192GB SOCAMM2 customer sampling for AI data centers

Earnings: Beat expectations for 9 consecutive quarters

Options Market Volatility

Extremely heavy unusual options activity, particularly around earnings dates

Large volume of $200-$250 calls for Jan/Feb 2026

Significant put buying at $180-$200 strikes (hedging)

Dec expiration showing high activity around $220-$240 strikes

Premium paid on some sweeps exceeding $1M

This suggests institutional players are positioning for continued volatility but with bullish bias.

Bottom Line

Micron Technology (MU) is the undisputed memory play of the AI Supercycle, driven by its technological leadership in High Bandwidth Memory (HBM), where it is one of only three global suppliers. The bull case rests on exceptional earnings growth fueled by AI demand, a critical competitive edge in next-gen tech like HBM4 and DRAM, and the significant geopolitical moat of being the sole U.S.-based major memory manufacturer. This momentum is validated by strong company guidance and accelerating analyst upgrades, suggesting the fundamental growth runway extends deep into 2026.

However, the stock’s massive rally has resulted in a stretched valuation. The downside risks are substantial. Investors must contend with the effective loss of the China market as a major revenue headwind and the risk of significant profit-taking after the stock has doubled. Furthermore, the name is highly vulnerable to violent whipsaws, as demonstrated by the sharp -26% drop in November, proving it is a purely momentum-driven stock sensitive to any moderation in AI spending or renewed trade/tariff uncertainty. While the HBM story is real and the fundamentals support continued expansion, the combination of aggressive insider selling and competitive threats from subsidized Chinese rivals means investors are paying a premium for growth, with little margin for error.

***

Disclaimer: This content is for informational purposes only and does not constitute financial advice. All opinions expressed are my personal views. Always do your own research and consult with qualified professionals before making investment decisions.

***

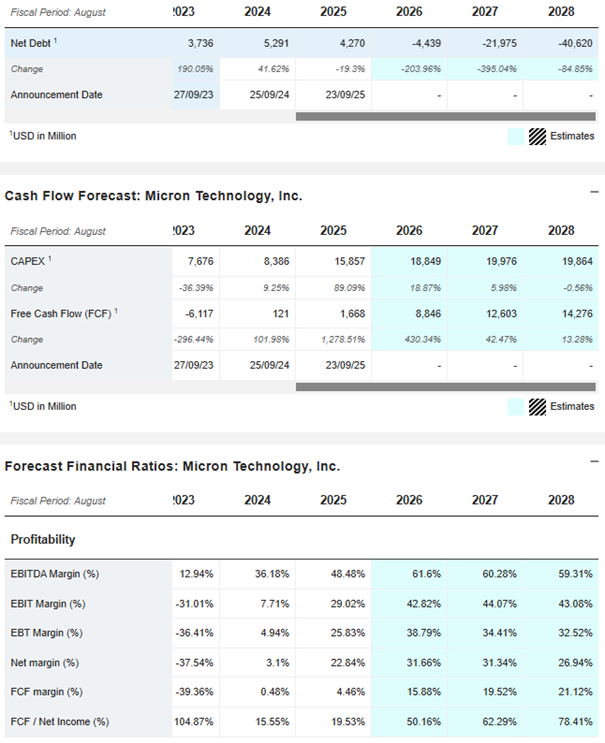

Appendix 1: Financial Projections:

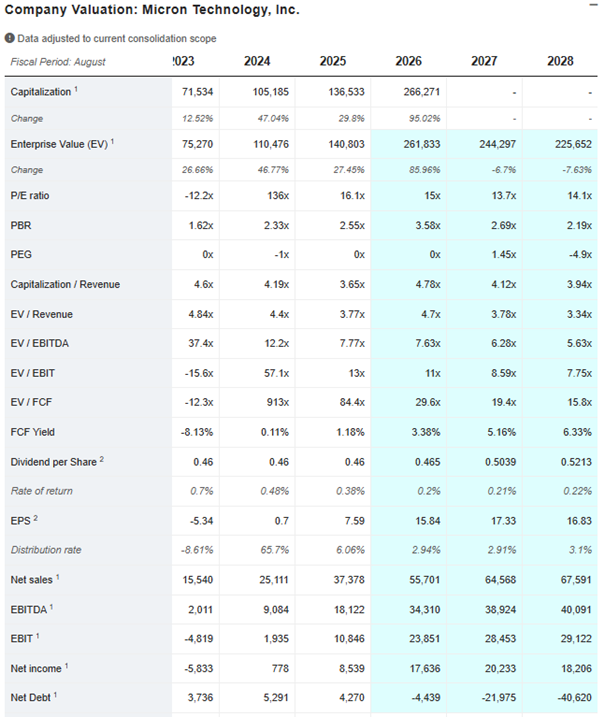

Appendix 2: Valuation Metrics:

Comprehensive article! Good information even for me, I can’t stay updated with everything all the time!

Micron (MU) remains a Strong Buy.

- Structural memory shifts reduce cyclicality and boost long-term demand visibility.

- Recent pullback (higher CAPEX, TurboQuant headlines, Sora shutdown) is short-term noise.

- Five-year SCA deals and consistent earnings beats support sustained demand and stability.

- Overcapacity and efficiency risks exist but show no signs of disrupting demand.

- At a P/E of 6.60x and a 3Y PEG of 0.05x, the stock trades at a steep discount to peers while offering significant upside potential