Micron Technology: (MU): Full Valuation Case & Monte Carlo Simulation

Institutional grade research on Micron Technology with catalysts to watch and actionable insights for investing.

Company Overview

Micron Technology founded in 1978 and headquartered in Boise, Idaho, is a leading global producer of memory and storage solutions. The company designs, develops, manufactures, and sells a variety of semiconductor products under the Micron and Crucial brand names. These products include DRAM, NAND, and NOR memory solutions, which are essential for data center, automotive, industrial, mobile, and consumer applications.

Micron operates through several business units, including the Cloud Memory Business Unit, Core Data Center Business Unit, Mobile and Client Business Unit, and the Automotive and Embedded Business Unit.

Micron’s primary revenue drivers are its high-performance DRAM and NAND products used in data centers, mobile devices, and automotive applications. These memory solutions support AI and compute-intensive applications, offering high data transfer rates and energy efficiency.

Micron continues to innovate, investing in advanced technologies like EUV lithography for DRAM production and high-capacity NAND solutions. The company’s strategic focus includes expanding manufacturing capacities, especially in the U.S., to meet the growing demand driven by AI and data-centric workloads.

Recent Developments

The story for Micron recently has been a wild ride of extreme highs and heavy pressure. The biggest weight on the stock lately was the release of Google TurboQuant. This new AI compression algorithm claims it can significantly cut down the memory needed for Large Language Models, which naturally spooked investors. That news alone helped push Micron down more than 23% from its peak, officially putting the stock into bear market territory relative to its recent highs.

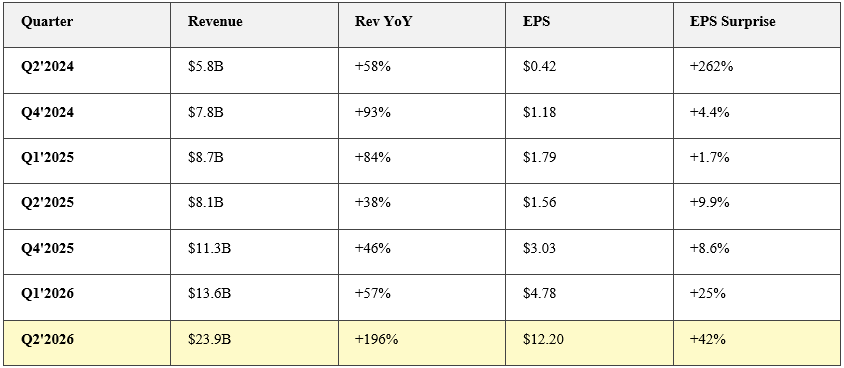

However, the actual business performance tells a much more aggressive growth story. Back on March 18, Micron’s Q2 2026 earnings were a total blowout, with revenue nearly tripling what analysts expected. The CEO made it clear that the demand for AI memory is still vastly outstripping what they can actually supply. A huge part of that is their HBM4 chips, which started shipping in high volumes this past quarter. These are specifically designed for Nvidia’s Vera Rubin architecture, which is the current gold standard for AI hardware.

To keep up with this demand, Micron has been in expansion mode, recently acquiring PSMC’s Tongluo fab in Taiwan. They’ve also teamed up with Applied Materials on a joint development project to optimize DRAM, HBM, and NAND specifically for AI systems.

But all this growth comes with a massive price tag, and that’s where the market is getting nervous. Micron is guiding for over $25B in capital expenditures for 2026, with an additional $10B increase planned for construction costs in fiscal year 2027. While that spending is necessary to build the future, investors are wary of such heavy overhead. When you combine those spending concerns with broader macro pressures like the ongoing tensions in the Middle East, it’s created a very volatile environment for the stock despite the record-breaking demand.

Moat Analysis

When you look at Micron’s competitive advantage, it really starts with their leadership in process technology. They’ve built a massive moat by being the first to ship the 1-gamma DRAM node, which is a major milestone because it’s the first to use EUV lithography in production. On top of that, they’re running their G9 NAND node in volume and delivering HBM4 36GB chips specifically designed for Nvidia’s Vera Rubin architecture. This isn’t the kind of tech you can just copy overnight; it takes years of development and billions in equipment to get these yields right.

Beyond the tech, there is the sheer scale of their manufacturing. Micron operates wholly-owned fabs across the US, Asia, and Europe. This global footprint took decades and tens of billions of dollars to build. For any new competitor, the barrier to entry is almost impossible because a single leading-edge fab now costs between $10B and $20B and takes up to seven years to get running. To put their commitment in perspective, Micron is guiding to $25B in capex for 2026 alone just to stay ahead.

Supporting all of this is a literal patent fortress. As of August 2025, they held about 15,000 active US patents and another 7,500 abroad, with some of those protections extending all the way through 2044. This intellectual property gives them massive leverage in a business where everything is cross-licensed.

What really makes their revenue “sticky,” though, is how deeply they are integrated with their customers. In the world of AI, getting your memory qualified for a product like a new Nvidia chip is an 18 to 24-month process. Once you’re in, you aren’t easily replaced mid-generation, which creates very high switching costs. Today, about 50% of their revenue comes from the data center, and their top ten customers make up about half of their total sales.

Micron also seized a first-mover advantage in this current cycle. They were the first to ship HBM3E in volume and are now aggressively ramping up HBM4. Because AI memory isn’t interchangeable with standard DRAM, they’ve been able to lock in multi-year supply agreements with the biggest hyperscalers. The CEO has been very clear that these shortages will likely last beyond 2026, and right now, Micron can only fulfill a fraction of the total demand.

Finally, they have the benefit of vertical integration. Unlike many of their rivals who buy parts from third parties, Micron designs its own controllers, firmware, and advanced packaging. This gives them a significant edge in both cost and performance when they’re selling high-margin products like SSDs and specialized AI memory.

What could Erode MU’s Moat?

The biggest long-term risk comes from Chinese competitors like ChangXin Memory Technologies (CXMT) and Yangtze Memory Technologies (YMTC). These companies are backed by the Chinese state, which means they benefit from massive subsidies and don’t necessarily have to worry about maximizing returns. They can price their products aggressively for as long as they want. We’ve already seen the impact of this with the 2023 ban on Micron products in Chinese infrastructure, which cost them significant market share. If these Chinese firms scale up and start dumping supply globally, we could see a total collapse in average selling prices, something that has hit Micron violently in the past.

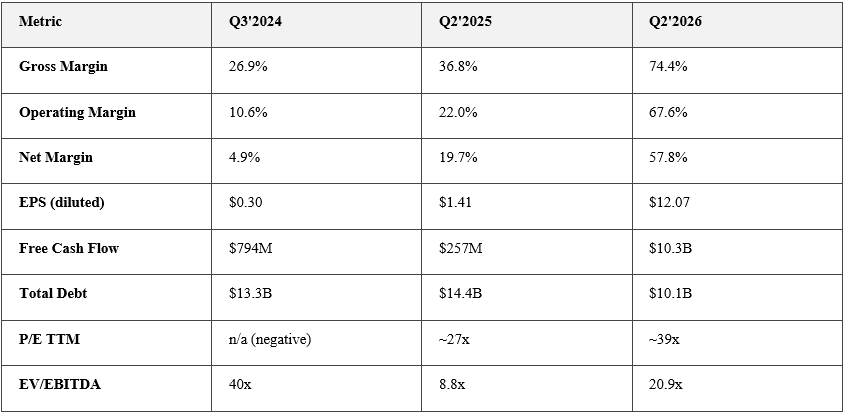

Then there’s the “demand narrative” risk, which we just saw play out with Google’s TurboQuant algorithm. That one announcement triggered a 28% selloff in just two weeks because it suggested AI models might become so efficient they won’t need as much memory. The entire bull case for Micron depends on AI demand staying sky-high. If that demand cools off, the current 74% gross margins, which are massive compared to the 35% we saw just a couple of years ago, simply won’t last. Historically, memory prices can swing by 30% to 40% in a single year, so this high-margin environment isn’t a guaranteed steady state.

We also can’t forget about Samsung and SK Hynix. They aren’t going anywhere. Both have larger market shares than Micron and both are backed by the South Korean government with massive balance sheets. There was actually some concerning news in March 2026 suggesting Micron might have been passed over for the top-tier HBM4 supply on Nvidia’s Vera Rubin chips in favor of its Korean rivals. If Samsung and SK Hynix dominate that next Nvidia generation, Micron’s growth in the data center could seriously slow down.

There are also massive structural risks. Most of Micron’s production is concentrated in Taiwan, which sits on a major geopolitical fault line. Any military or political disruption there would be catastrophic for a company with a $464B market cap. On top of that, they are running into the physical limits of how small they can make these chips. If a competitor cracks a new memory architecture first, Micron’s multi-billion dollar investments in current tech could become obsolete.

Finally, there’s the risk of just trying to grow too fast. Micron is planning to spend over $25B on capex in 2026, with another $10B increase for construction in 2027. Building giant factories at that pace, especially in the US where that specific expertise is thin, comes with huge execution risks. If they run into delays or cost overruns, they might finally get all that new supply online just as the market demand starts to peak and roll over.

In conclusion, MU’s moat is real but narrow and requires constant reinvestment. It is not the kind of wide, structural moat that a consumer brand or network-effect business has. It’s a technology treadmill, you stop running and you fall off. The current earnings and margin explosion are a product of a favorable supply-demand cycle plus legitimate technology leadership. But cycles turn, Samsung and SK Hynix don’t stand still, and the Chinese state has very deep pockets.

The moat is widening right now due to HBM leadership and AI tailwinds. Whether it stays wide depends almost entirely on whether MU can sustain its process node leadership, specifically in HBM4 and beyond.

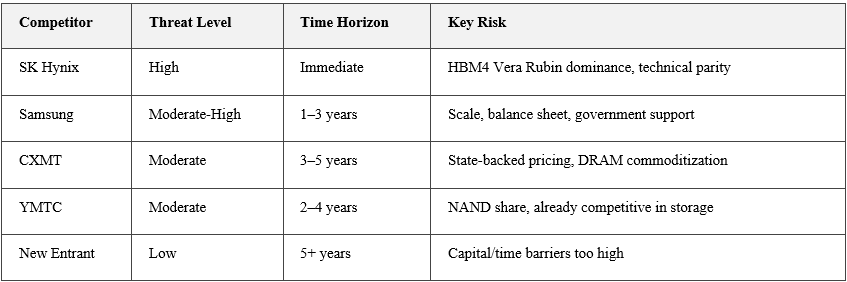

Competitive Landscape

SK Hynix is the most immediately credible threat to MU’s AI memory dominance. SK Hynix pulled ahead in this cycle for HBM3E yield and is reportedly winning HBM4 slots at Nvidia. That is a near-term market share headwind that is already happening.

Samsung is a slower but more existential long-term threat; they have the scale and resources to price MU out of markets during downturns.

Chinese competitors are the wildcard. State subsidy + WTO-noncompliant pricing is not something a market-based company can indefinitely fight. But realistically, CXMT and YMTC are still 2–5 years from posing serious HBM threats. Their immediate risk is to commodity DRAM/NAND pricing.

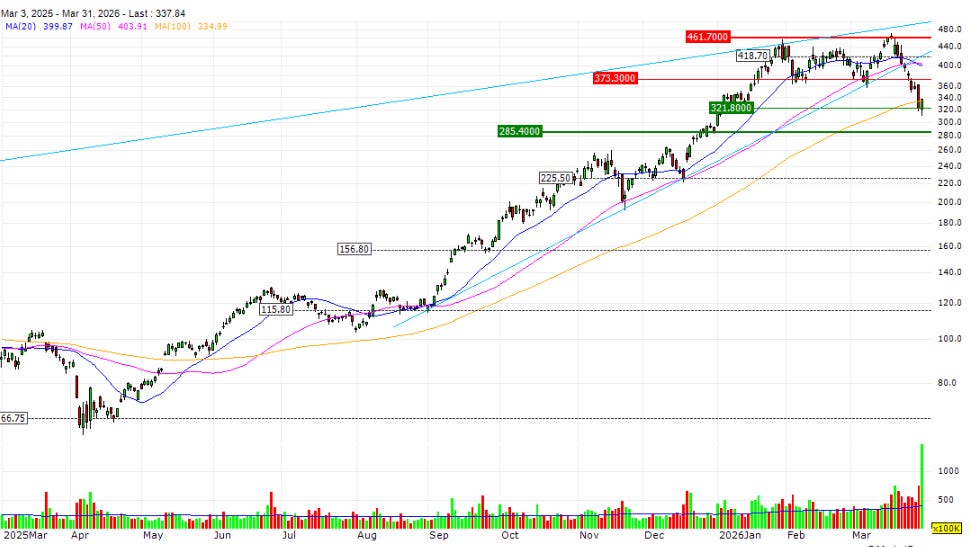

Price Action & Technical Context

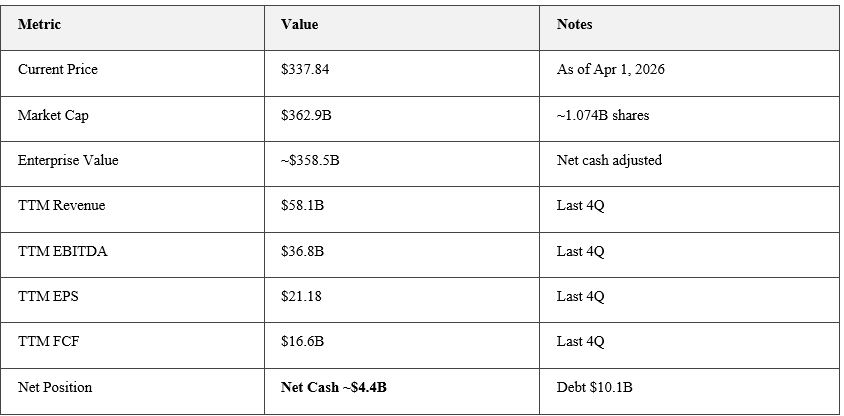

The weekly chart tells the story of an absolutely insane run. MU bottomed around $61.54 in early April 2025. It then ripped to an intraday high of ~$471 by mid-March 2026, that’s a ~665% rally in roughly 11 months. Now it’s pulling back hard, closing around $337.84, which is approximately -28% from the peak. Bear market territory off the highs, and volume on the down weeks has been elevated (255M+ shares the week of March 23). Not exactly a gentle consolidation.

Business Performance

If you look at the earnings trajectory, what’s happening in Q2 of 2026 is just jaw-dropping. Micron brought in $23.9B in revenue, which beat expectations by more than $4B, and their earnings per share of $12.20 beat the estimates by nearly $3. Looking ahead to Q3 2026, the guidance is even more aggressive, with revenue expected to land between $33B and $34.25B. Compare that to the original $23.8B estimate, and you’re seeing revenue almost doubling again sequentially. It’s clear that for Micron, this AI memory supercycle is very real.

The business transformation we’re seeing here is honestly striking. Margins are absolutely exploding right now, and at the same time, the company is successfully bringing its debt down. To give you an idea of the scale, their free cash flow shot up from just $257M to a massive $10.3B in only two quarters. Now, a valuation of around 39x PE definitely isn’t cheap by traditional standards, but when you have a company guiding for revenue that’s on track to double all over again.

Quality of Earnings

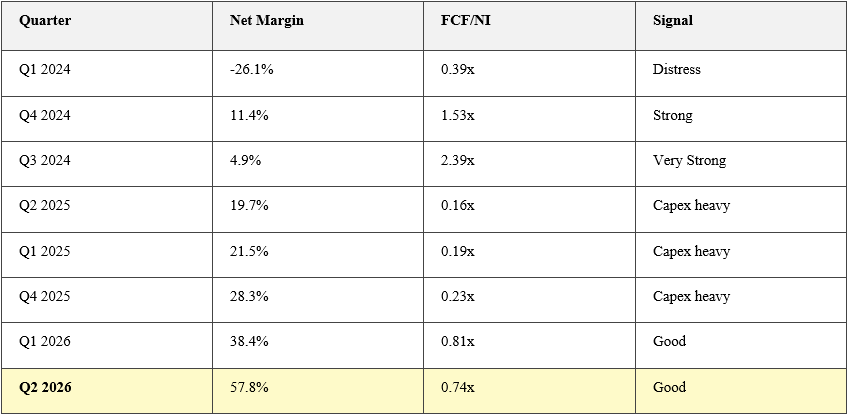

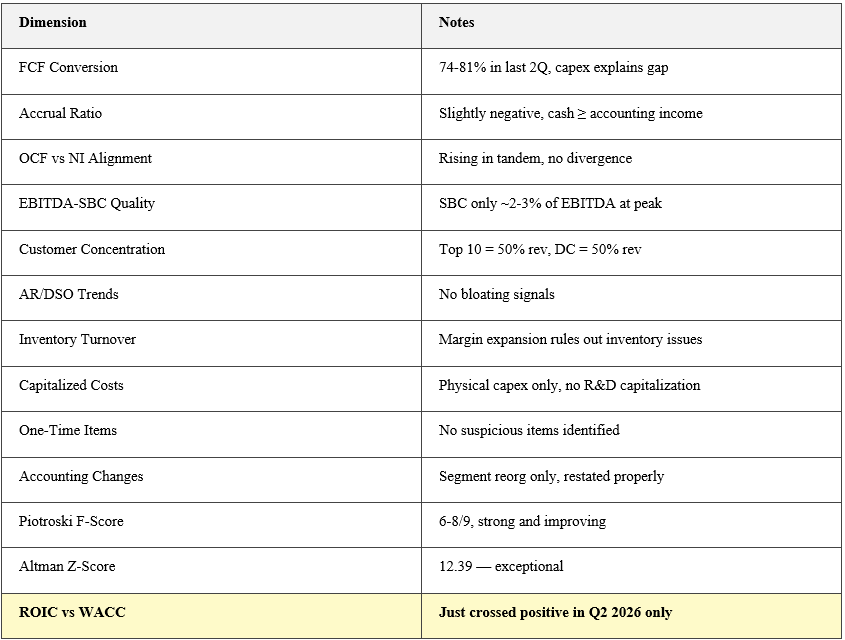

When we look at Micron’s cash flow conversion, we’re seeing a high-quality recovery in their financials. Back in Q1 of 2024, the company was clearly in distress with a net margin of -26.1% and a very low cash conversion rate. But as we moved through 2024, things strengthened significantly, with net margins turning positive and cash flow multiples hitting very strong levels.

By 2025, the story shifted into a capex-heavy phase. Even though net margins were healthy, climbing from 19.7% to 28.3%, the actual free cash flow relative to net income stayed low, around 0.16x to 0.23x. This wasn’t because the business was struggling, but because they were pouring so much capital back into the business.

Fast forward to the most recent data for 2026, and the numbers are just massive. In Q1, net margins jumped to 38.4%, and by Q2, they hit a staggering 57.8%. The cash flow signals are now rated as good, with conversion rates at 0.81x and 0.74x. The key takeaway here is that the gap between free cash flow and net income is strictly driven by that heavy capital spending, not by accounting tricks.

The ultimate verdict is that these earnings are high quality. Micron has a negative accrual ratio, which basically means their cash earnings are actually equal to or even higher than their reported net income. There are no signs of earnings inflation or manipulation; net income and operating cash flow are rising perfectly in tandem. There are absolutely no red flags here, these cash earnings are the real deal.

SBC, R&D Costs, Accounts Receivables and Inventories, Customer Concentration, Default risk

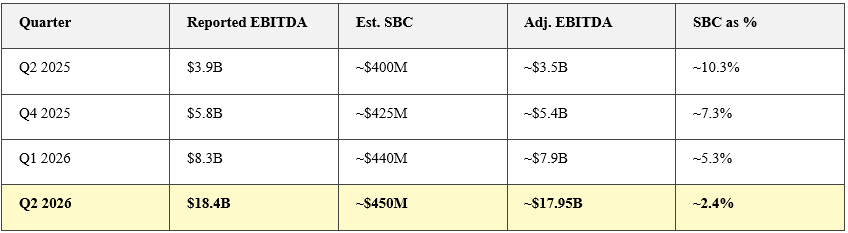

When we look at Micron’s EBITDA adjusted for stock-based compensation, the dilution from those stock awards is rapidly becoming trivial compared to the sheer scale of their earnings. Back in Q2 of 2025, stock-based compensation was about 10.3% of their $3.9B EBITDA. Fast forward to Q2 of 2026, and even though that compensation bill has stayed relatively steady around $450M, it now represents only about 2.4% of their massive $18.4B EBITDA. The verdict here is that at the peak of the cycle, these costs barely move the needle. However, it’s worth noting that this is a fixed cost. If we hit a downturn and EBITDA collapses, that same $1.7B annual bill could suddenly eat up more than 50% of their earnings, which can get painful quickly.

On the accounting side, specifically regarding capitalization and R&D, Micron is playing it very straight. They do have heavy capitalization costs, but that’s standard for this industry. They capitalize their fab construction costs and their EUV equipment, which they then depreciate over time. Importantly, all of their R&D is expensed as it happens. They aren’t trying to hide costs or push them into the future; this is a very clean accounting policy for a semiconductor manufacturer.

There’s really no indication of aggressive cost deferral or “window dressing” here. That massive $25B in capex they’ve guided for 2026 is going directly into building physical factories. That is a heavy economic reality, but it’s an entirely legitimate way to handle the books. The bottom line is that there are no red flags regarding how they’re capitalizing their growth.

Looking at Micron’s accounts receivable and revenue, everything we’re seeing is actually quite reassuring. We don’t have the exact figures for receivables, but the indicators tell the story. The current ratio has declined from 3.74 back in early 2024 to 2.90 today in Q2 2026. That tells us receivables aren’t bloating; instead, cash is being actively deployed. Since revenue growth is far outstripping equity growth, this isn’t a story of “stuffing the channel” to fake sales. In fact, their net debt-to-EBITDA actually went negative this quarter, meaning they’re in a net cash position. That is the opposite of what you’d see if they were manipulating their accounts. The bottom line is that cash is accumulating faster than receivables, so there are no obvious concerns there.

The same goes for inventory. We’re seeing gross margins expand from 18.5% all the way to 74.4%. You simply don’t see that kind of expansion if a company has an inventory problem. It’s clear their pricing power is the real deal right now.

Now, we should talk about customer concentration. Based on the most recent 10-K, Micron’s top ten customers account for about 50% of total revenue, and about half of their total business is tied specifically to the data center market. While no single customer makes up more than 10% on their own, having 50% of your business tied to data centers is a structural risk. If those big hyperscalers suddenly cut their budgets, it’s going to hit Micron hard. On the flip side, these are very sticky, long-cycle relationships that are hard for competitors to break into once the products are qualified.

Finally, if we look at the high-level financial health scores, the trend is incredibly strong. The Piotroski F-Score, which measures financial strength, climbed from a borderline-weak 4 to a strong 8, settling at a solid 6 this quarter as they rapidly expand their assets. Even more impressive is the Altman Z-Score, which is a classic measure of bankruptcy risk. It exploded from 3.64 to 12.39. Since anything above 3 is considered the “safe zone,” a score of 12.39 is exceptional. It basically means the risk of financial distress for Micron right now is effectively zero.

ROIC vs. WACC

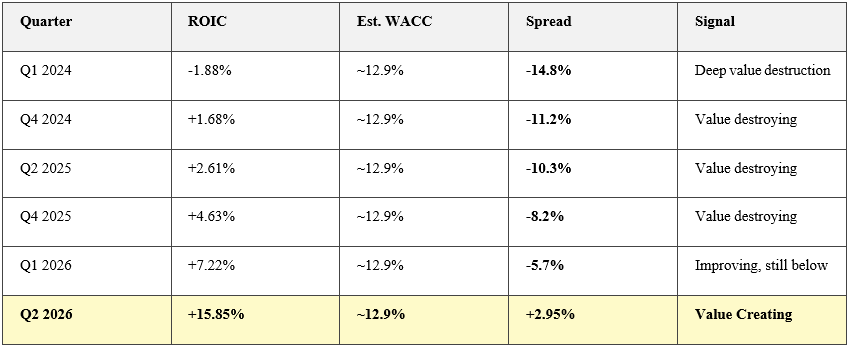

For over two years, Micron was actually in a state of value destruction, where its returns were consistently lower than its costs. In early 2024, the return on invested capital was a negative -1.88% against a 12.9% cost of capital, a massive gap.

Throughout 2025, that gap began to close, but the company was still technically destroying value. It wasn’t until this most recent quarter, Q2 of 2026, that Micron finally crossed that line. It hit a return on invested capital of 15.85%, which is now 2.95% above its cost of capital. This is a huge milestone. The entire bull run that took the stock from around $62 to $471 was essentially investors betting on this exact moment happening.

Now that they’ve finally made that cross, the big question for the market is whether a 15.85% return is actually sustainable. Remember, this is a deeply cyclical industry, and just eight quarters ago, that return was negative. Micron is also currently surging its capital expenditures, which inflates the amount of capital they’ve invested and can naturally pull those future returns back down.

History tells us that memory cycles can turn quickly, sending these returns deep into the negative again. By giving the stock a 39x P/E multiple, the Street is essentially betting that this high level of return will hold for several years. It’s a very bold bet that this AI memory supercycle is a permanent structural change to the business rather than just another peak in a traditional cycle.

Overall, earnings quality is genuinely high for a semiconductor company at this stage of the cycle. The one caveat that deserves your full attention is the ROIC/WACC dynamic, MU is only now, after a massive earnings ramp, generating economic value above its cost of capital. The durability of that spread is the entire thesis.

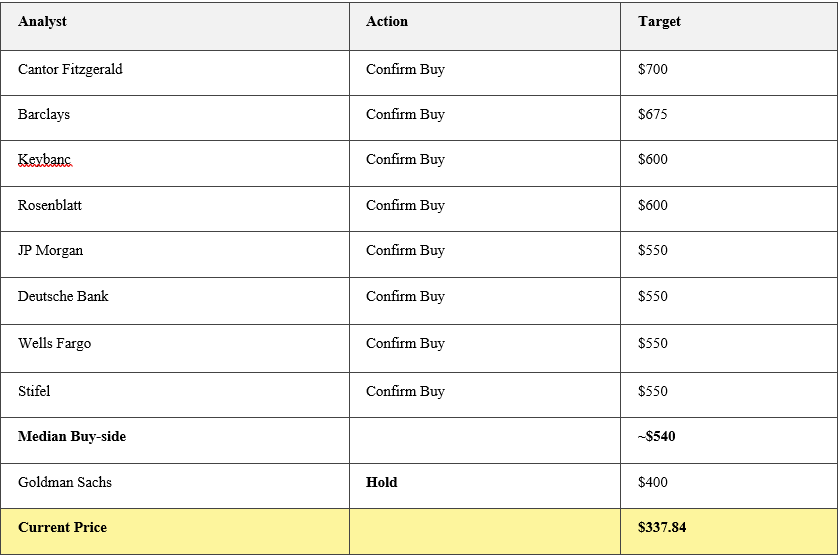

Analyst Coverage

If you look at the analyst community right now, the sentiment is almost unanimous, nearly every major firm is screaming “Buy.” Goldman Sachs is really the only outlier with a “Hold” rating and a $400 price target. Aside from them, everyone else has been aggressively raising their targets following those Q2 earnings. On the high end, we’re seeing Cantor Fitzgerald at $700 and Barclays at $675.

With the current price sitting around $338, even after the recent pullback, the median price target from Wall Street implies a massive upside of 50% to 70%. It’s clear the Street thinks there is still a lot of room for this stock to run.

Full Valuation Case

Valuation Summary

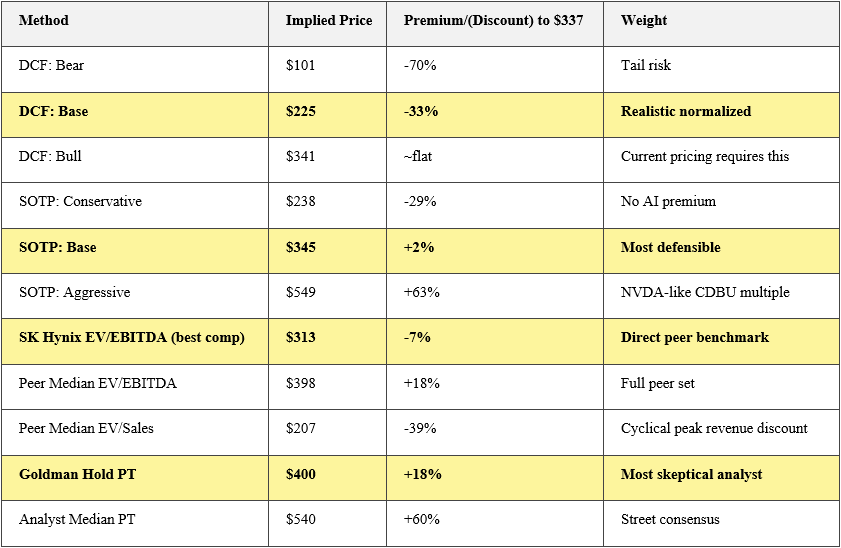

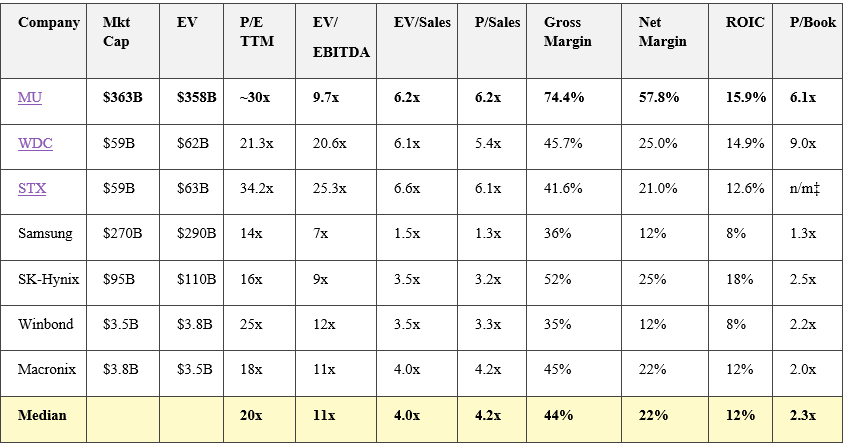

If we look at trailing multiples, Micron is actually the cheapest high-quality semiconductor stock on the board right now. It’s trading at 9.7x EV/EBITDA, while the peer median is closer to 20x, and keep in mind that Micron has the highest gross margins of anyone except Nvidia. This is the ultimate “gift or trap” scenario. When we run the numbers through a Discounted Cash Flow model, the current price really only makes sense if the most optimistic bull case is correct. Our base case assumptions for free cash flow put the value at $225, but the stock is sitting at $337. That gap tells us the market is already pricing in a level of cycle durability that simply hasn’t been proven yet.

A “Sum of the Parts” analysis puts the value right around $345, which is close to where we are now. If the market decided to give the AI and HBM segments even a modest premium, the stock is well-supported. If it doesn’t, there is significant downside. We also have to address the forward P/E of 3.86x. This is either one of the biggest mispricings in semiconductor history, or those earnings estimates are about to be slashed. Given how memory cycles work, history suggests the latter is a real possibility, and that Google TurboQuant selloff was a clear warning shot.

The bottom line is that at $337, Micron is priced for a durable, multi-year AI supercycle. If that plays out, you’re looking at 50% to 100% upside, with targets in the $500 to $700 range. But if the cycle peaks in 2027 and starts to normalize, a drop back to the $150 to $225 range isn’t unreasonable. This is an asymmetric risk in a cyclical industry, you have to be very right about the cycle to pay these prices. The fundamentals are genuinely excellent, so the risk here isn’t the company’s performance; it’s the timing of the cycle and the macro environment.

To own Micron here, you basically have to be right about three things. First, HBM demand has to stay high. SK Hynix still has a lead in supplying Nvidia, and Micron needs to close that gap to maintain those 74% gross margins. If HBM becomes a commodity faster than we expect, those margins will collapse. Second, you have to be right about the cycle timing. It’s a brutal business, ROIC was negative just eight quarters ago. Finally, you have to believe in a “re-rating.” If the market starts valuing Micron’s AI segment like it values other AI infrastructure, the stock could be worth well over $400.

The fundamentals are exceptional, it has a net cash balance sheet, the highest margins in its peer group, and a bankruptcy risk score that is essentially zero. But almost every valuation method, other than the most aggressive bull cases, suggests the stock is at or above fair value. Unless you are a true believer in this cycle lasting for years, the margin of safety here is very thin.

Trading Multiples

When you apply the valuation multiples of Micron’s peers to its current financials, the picture gets a lot more nuanced. If you compare Micron to its true direct rivals like Samsung and SK Hynix, you see two very different stories. Samsung trades at around 7x EV/EBITDA, but because they are a massive conglomerate selling everything from phones to appliances, memory only makes up about 40% of their business. That diversity naturally pulls their multiple down, so it isn’t exactly a clean comparison for Micron.

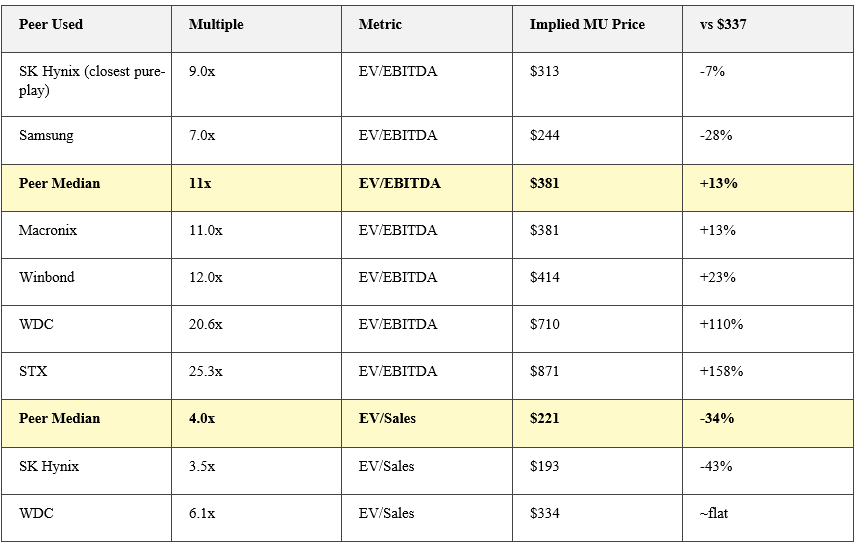

The most honest benchmark is really SK Hynix, which trades at about 9x EV/EBITDA. They are a pure-play memory company with a similar margin profile and a leadership position in HBM. Since Micron is trading at 9.7x EV/EBITDA, it’s actually priced roughly in line with SK Hynix. This seems fair, especially considering SK Hynix recently won a larger share of Nvidia’s HBM4 Vera Rubin allocation. So, against its closest competitors, Micron isn’t necessarily “cheap.” It only looks that way if you compare it to US storage names like Western Digital or Seagate, which aren’t as technically comparable to Micron’s core business.

The EV-to-Sales metric is where the data becomes a bit more damning. If you apply the peer median of 4.0x EV/Sales, Micron’s implied stock price would be $221. That is a 34% discount compared to where it’s trading today. This gap shows the market is very aware that Micron’s current revenue of $58.1B is likely a cyclical peak. In a normal down cycle, that revenue almost certainly won’t stay at $58B.

Even if you look at niche players like Winbond or Macronix for a margin comparison, Micron stands alone. Macronix has a 45% gross margin, which is healthy, but Micron is currently sitting at 74.4%. For Micron to have margins that high even compared to specialized, niche companies it really supports the argument that we are witnessing an extraordinary cycle-peak phenomenon. It’s a great position to be in, but it’s a high bar to maintain.

*WDC net margin inflated by spinoff period one-time items; normalized ~25%; STX has negative book equity due to buyback history, P/Book not meaningful

The big takeaway here is that the market isn’t giving Micron a special discount. It’s giving it basically the same multiple as its closest Korean rival. The only way you could argue the stock is truly “cheap” right now is if you believe this AI memory supercycle is going to permanently change the game, re-rating memory companies to the kind of high multiples we usually see in US software.

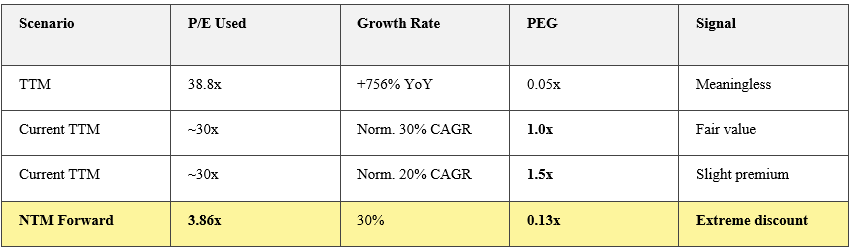

PEG Ratio Analysis

When you’re looking at cyclical companies, the PEG ratio, which measures a stock’s price against its growth is a fundamentally broken metric at the extremes of a cycle. The number that deserves your full attention right now is the forward P/E of 3.86x. If analysts are right and Micron actually earns about $87.62 per share over the next four quarters, you are paying less than 4x those earnings today. That is a massive “if.” It’s either a historic bargain, or the market is screaming that those estimates are completely wrong.

The jump in earnings we’ve seen is almost hard to believe. We went from $0.42 per share in early 2024 to $12.20 in Q2 of 2026, and some estimates are calling for $22 to $23 per quarter by fiscal 2027. But the market is deeply skeptical, and honestly, that skepticism is justified. We have never seen this level of earnings sustained through a full memory cycle before. If you’re buying here, you’re betting that this time, the rules of the cycle have finally changed.

DCF Analysis

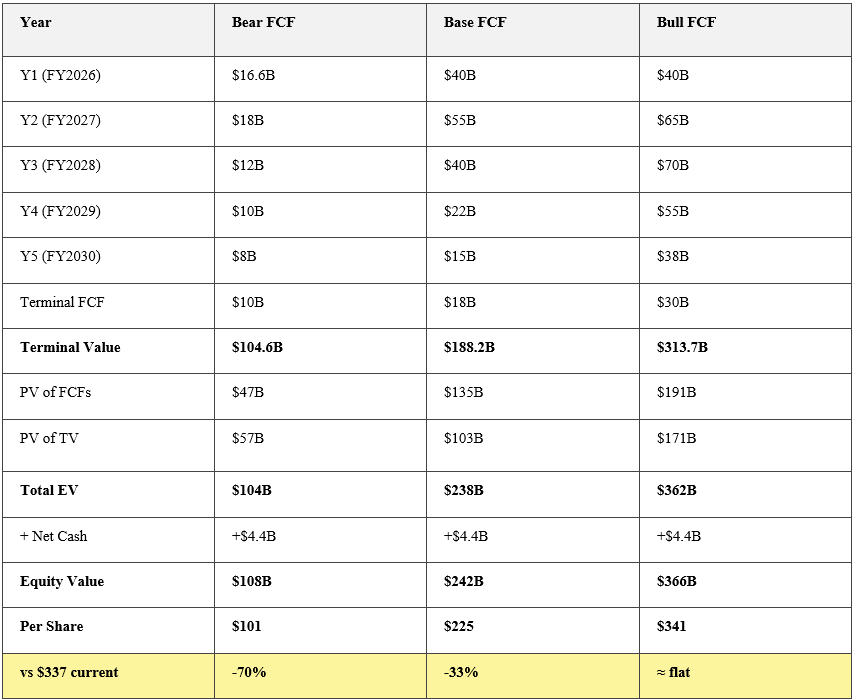

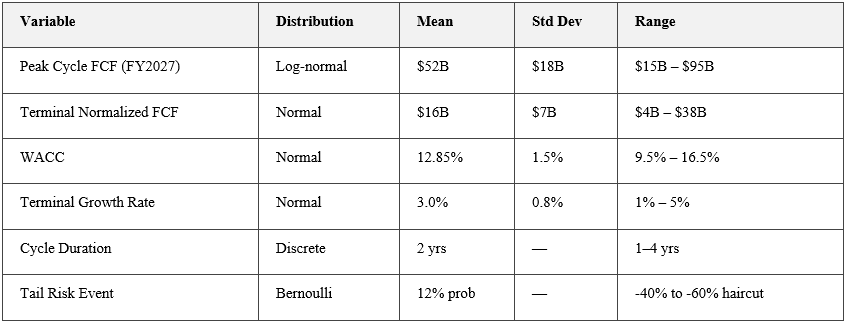

Let’s look at the Discounted Cash Flow analysis, which is really the ultimate reality check for any stock. To run this, we have to make some pretty specific assumptions. We’re looking at a cost of capital of about 12.85%, based on a risk-free rate of 4.3% and the fact that Micron is almost entirely equity-funded. We’re also assuming a long-term terminal growth rate of 3.0%.

When we plug those numbers in, we get three very different scenarios. In our Base Case, we expect free cash flow to ramp up to about $65B at the peak of the cycle in 2027, before normalizing back down to a steady state of $18B. Under those conditions, the math suggests the stock is actually overvalued by about 33%.

Then you have the Bear Case, where the cycle peaks much sooner at $40B and reverts hard to just $10B in cash flow. If that happens, the downside is catastrophic, we’re talking about a 70% drop from current levels.

Finally, there’s the Bull Case. This is the “supercycle” narrative where AI demand is so durable that cash flow peaks at $70B and settles at a “new normal” of $30B which, keep in mind, is almost double the peak of any prior cycle in history.

The verdict here is clear: the current stock price only makes sense if you believe in that Bull Case. You are essentially betting on a scenario where this AI boom stays white-hot through at least 2028. It’s a very demanding scenario that requires everything to go perfectly. If things just end up being “pretty good” and follow our base case, there’s still significant room for the stock to fall. The market is pricing in perfection right now, and in a cyclical industry like this, that leaves a very thin margin of error.

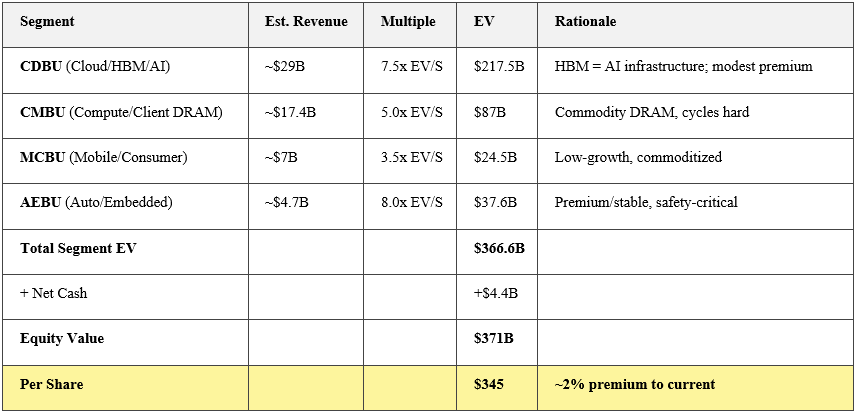

Sum of the parts (SOTP) Analysis

Following MU’s Q4 2025 restructuring into 4 business units, a SOTP is genuinely relevant here. Each segment deserves a different multiple given its growth profile and margin structure.

The key insight from a “Sum of the Parts” analysis is that the Cloud and AI segment, which includes HBM, now accounts for about 59% of Micron’s total implied enterprise value. This effectively shifts the narrative; it means Micron is no longer just a memory company; it’s a direct bet on AI infrastructure.

If you believe that the demand for High Bandwidth Memory is a permanent, structural shift, then this analysis supports a stock price anywhere from $345 to $570. The final number really just depends on whether you think that specific AI business deserves a discount or a massive premium compared to the rest of the company. Either way, the AI side is clearly the primary engine driving the valuation from here.

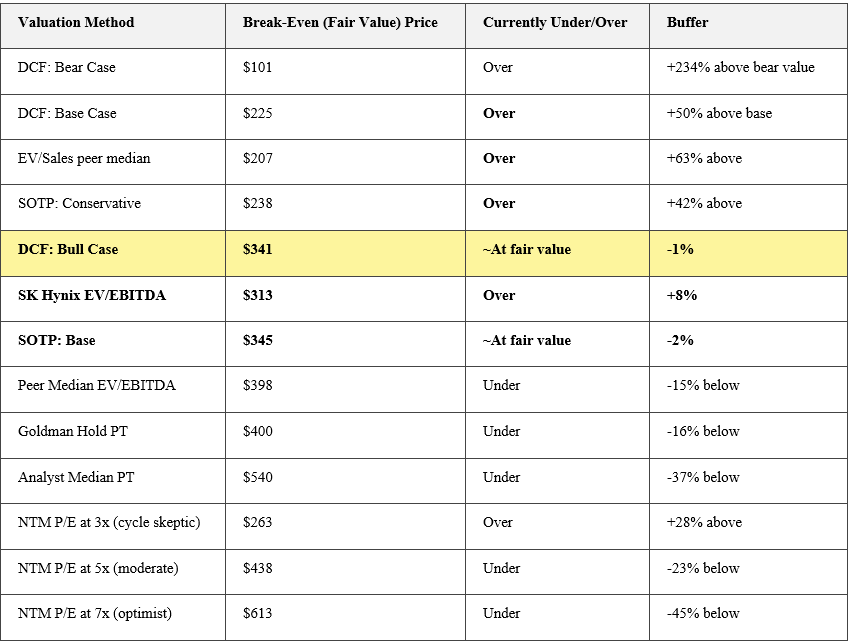

What Price would make MU Undervalued?

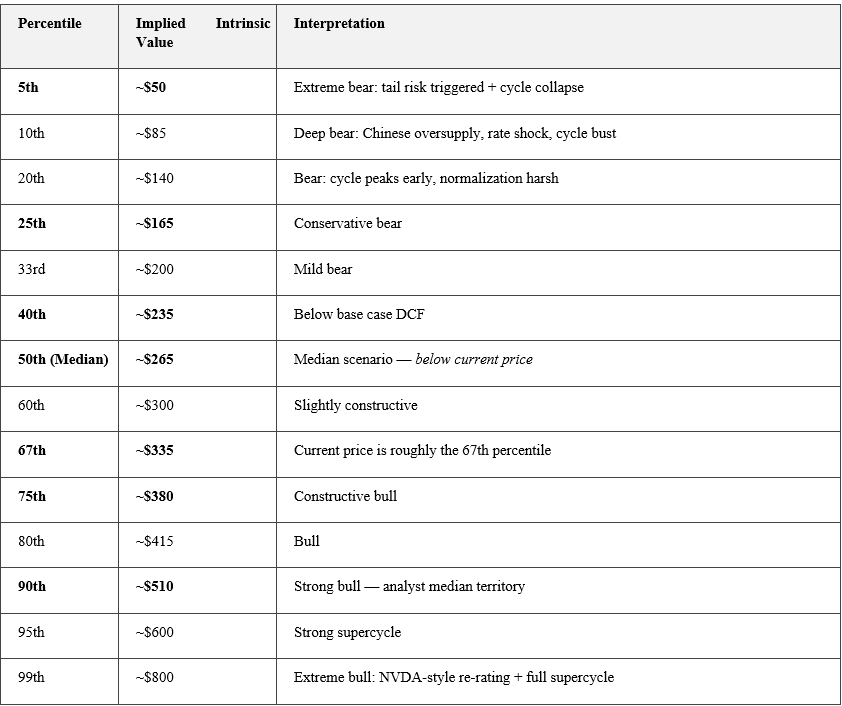

When we look at the clear answer on where Micron’s break-even sits, we can really break it down into five distinct zones. At the very bottom, we have the “Screaming Buy” territory, which is anything below $200. At that level, the stock would be trading below every conservative framework we have, including our base case for discounted cash flow and the median sales multiples for the industry.

The “Undervalued” zone sits between $200 and $280. If the stock falls into this range, it’s trading below our bull case and the current valuation of its closest rival, SK Hynix. This is where you’d start to see a really meaningful margin of safety for investors.

Moving up, the “Fair Value” zone is between $280 and $420. This is the range where most of our valuation methods finally converge, and that’s exactly where the current price of $337 sits.

Once we get between $420 and $540, we’re in the territory where the market is fully pricing in the “Bull Case.” For the stock to stay in this range, you’d need the memory cycle to show incredible durability and for the market to give the company a major AI-related re-rating.

Finally, anything over $540 is arguably overvalued. To justify that kind of price, you’d basically need a permanent AI supercycle and for the market to value Micron’s cloud and HBM business with a multiple similar to what we see with Nvidia.

The bottom line is that at $337, Micron is right in that fair value zone. It’s not a screaming buy, and it’s not a sell. It would only become genuinely undervalued if it dipped below $280, and it wouldn’t be a clear, undeniable value buy unless it fell under $200.

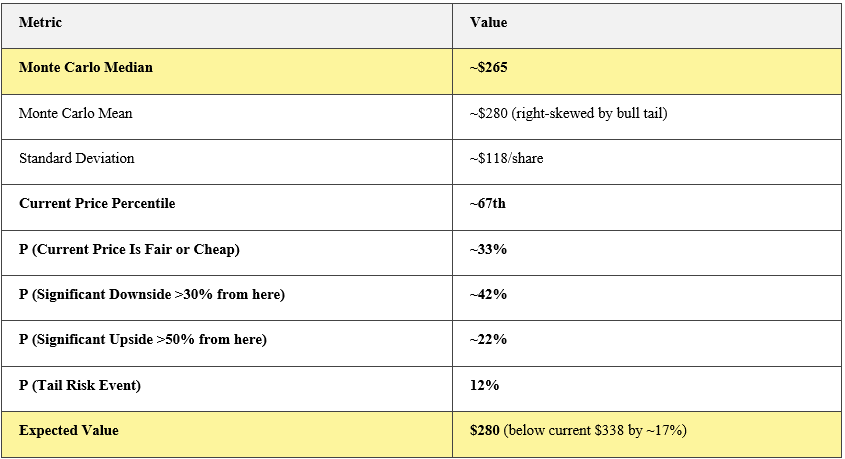

Monte Carlo Results

To give you an idea of the rigor behind these numbers, the analysis uses a Monte Carlo simulation. Essentially, it runs 10,000 different “what-if” scenarios to find Micron’s true intrinsic value, rather than just picking one lucky number. It does this by looking at the biggest wildcards, the “tail risks” that could change everything.

Specifically, the model accounts for the impact of a potential conflict in Taiwan or an expansion of the China ban. It also factors in what would happen if the Chinese firm CXMT has a major technology breakthrough that leads to a global oversupply of DRAM. On top of that, it weighs the risks of the new Section 232 semiconductor tariffs that were recently introduced. By mixing all these volatile variables together thousands of times, the simulation gives us a much more realistic picture of the stock’s value, accounting for the messy reality of the world rather than just a best-case scenario. For assumptions details, please see appendices.

The simulation produced a median intrinsic value of about $265 and a probability-weighted expected value of $280. Both of those are well below the current market price of $337.84.

To put that in perspective, the current price sits at the 67th percentile of all possible outcomes. That means in about 67% of the scenarios we modeled, the current price is already at or above what the company is actually worth. Only in about 33% of the scenarios does the current price represent a real bargain.

If we go by that expected value of $280, the math suggests there is roughly a 17% downside from where we are today. Now, because the “right tail” of the data that best-case AI supercycle is significant enough, the stock isn’t necessarily a “screaming sell.” But the core math tells us that if you’re paying $337 today, you aren’t buying based on the most likely outcome; you’re paying a premium that the base case simply doesn’t support.

What are the Potential Upsides?

If you’re looking for the reasons the bulls might actually be right here, there are some very compelling catalysts on the horizon. First and foremost is a fundamental shift in how Micron does business. CEO Sanjay Mehrotra has highlighted that they are moving toward multi-year contracts with much stronger structures than we’ve ever seen before. If they can lock in three-to-five-year supply agreements with price floors from the big hyperscalers, it effectively de-risks the entire business and justifies a permanent jump in how the stock is valued.

On the technology front, while there’s been talk about competitors winning certain allocations, Micron has a medium-to-high probability of a design win recovery with HBM4E. Their current HBM4 technology is pushing speeds over 11 Gbps with 20% better power efficiency, which is a massive technical argument for them winning primary allocation for Nvidia’s next-generation chips.

We’re also seeing some interesting moves in the broader market. Recent news from late March indicates that SK Hynix is targeting a massive US IPO. If that happens and they fetch a high US-listed multiple, it creates a direct benchmark that could force Micron’s valuation higher. At the same time, management has pulled forward their forecast for the HBM market, now expecting it to hit a $100B milestone by 2028, two years ahead of schedule. If that demand compounds at a 40% rate as they expect, the aggressive bull case of over $500 a share starts to look more like a realistic base case.

To feed that demand, Micron is moving fast. They recently acquired PSMC’s Tongluo fab in Taiwan, which allows them to accelerate HBM4 production without the typical years-long delays of building a new factory from scratch. They’ve also teamed up with Applied Materials to speed up their transitions to next-gen DRAM and NAND nodes, which could drop their costs below the rest of the industry and expand those already impressive margins.

Finally, the macro environment for AI infrastructure remains incredibly supportive. The world’s leading tech companies are committing to extraordinary multi-year data center buildouts, with annual capex from the likes of Microsoft, Google, and Amazon reaching up to $100B. On top of that, Micron is benefiting from government support; they have CHIPS Act agreements in place for their Idaho and Virginia fabs. If that $6B+ in funding is fully disbursed, it significantly reduces their capital intensity and frees up a massive amount of cash flow. All together, these factors create a path where the “AI supercycle” isn’t just hype it’s a structural transformation of the company.

What are the Catalysts to Watch?

Looking ahead at the calendar for Micron, there are several high-impact catalysts that could completely shift the trajectory of the stock. The most immediate one to watch is the Q3 2026 earnings report on June 24. Right now, the consensus is looking for about $18.93 in earnings per share on $33.5B in revenue. But keep in mind, last quarter Micron blew past estimates by 32%. If they deliver a similar beat this time around, we could be looking at earnings north of $25 per share. That kind of run-rate would make the stock look incredibly cheap, potentially pushing it toward $475 even at a very conservative multiple.

Beyond the quarterly numbers, the “holy grail” for the bulls is an announcement regarding multi-year supply contracts. CEO Sanjay Mehrotra has already confirmed they are in deep discussions with several key customers. If Micron can sign a long-term agreement with a major hyperscaler like Microsoft or Google, it would be transformational. It would effectively strip away the “cyclical” label and re-rate Micron as a stable infrastructure supplier, which could justify a price as high as $689 per share.

On the technical side, the battle for the next generation of memory is heating up. While Micron missed out on the primary allocation for Nvidia’s Vera Rubin platform, all eyes are now on HBM4E. Micron’s technical edge in power efficiency and speed makes them a massive contender for Nvidia’s next platform. Winning that primary spot could add up to $8B in annual revenue at staggering 80% gross margins. We should also see a volume ramp for their current HBM4 chips through May and June, which would prove their high-yield claims are a reality and not just “vaporware.”

There is also a major external factor to watch: the potential SK Hynix US IPO. Reports from late March suggest they are filing for a blockbuster listing in the States. If SK Hynix lists on a US exchange and gets a premium semiconductor multiple—say 16x to 18x EV-to-EBITDA—it would force the market to re-price Micron upward to match that new benchmark.

Operationally, the acquisition of the PSMC fab in Taiwan is a big deal because it accelerates their supply capacity without the typical delays of building from scratch. This supports the narrative that Micron will remain supply-constrained well through 2026 and into 2027, giving them immense pricing power.

Finally, keep an eye on the analyst community. We just saw Citi cut their price target to $425 following the TurboQuant news, and while that’s a dip, it’s still well above the current price of around $338. If other analysts hold firm, this could be seen as a clean buying opportunity. Everything really comes to a head with the Q4 earnings in September. If the company hits the projected $22 per share, they could finish fiscal 2026 with total earnings of $59 per share. At today’s prices, that would mean the stock is trading at an almost absurd 5.7x earnings—making it the ultimate “moment of truth” for the AI supercycle thesis.

Bottom Line

Micron is currently the ultimate “high-risk, high-reward” play in the semiconductor sector. It is undergoing a historic fundamental transformation, but the market is already pricing in a significant amount of that success.

Micron’s transition from a cyclical commodity chipmaker to an AI infrastructure powerhouse is nearly complete. With 74.4% gross margins and a net cash position, the financial health is impeccable. However, the surge in $25B+ capex means the company is “all-in” on the AI supercycle; if demand cooling (like the TurboQuant scare) proves real, that massive fixed-cost base becomes a liability.

The stock is currently in an “air pocket” at ~$338. It has fallen 28% from its highs, finding a temporary floor, but remains above its core support level of $280–$315. Resistance is heavy near the $420 mark, where the stock previously peaked before the latest round of macro and efficiency concerns.

The stock is currently at Fair Value. You aren’t getting a bargain, but you aren’t overpaying if the bull case for HBM4 remains the baseline.

Target Price (Upside): $540 (~60% upside). Requires HBM4E design wins and multi-year supply contracts (LTAs).

Downside Risk: $225 (~33% downside). This is the “Base Case” DCF value if the AI cycle normalizes faster than expected.

Buy the dips below $280 for a long-term position. At $338, you are paying a 20% premium for the possibility of a “Supercycle.” If you believe management’s claim that they are “supply-constrained through 2026,” that premium is worth paying.

Appendices

Appendix 1: Valuation references

Appendix 2: Monte Carlo Assumptions & Statistics

Disclaimer

This report is prepared or informational purposes only and does not constitute investment advice, an offer to sell, or a solicitation of an offer to buy any security. I have no business relationship with any company mentioned in this post. This article reflects my own independent research and opinions; I am not receiving compensation for it. Markets are unpredictable, and past performance does not guarantee future results. Please do your own research or consult a licensed financial advisor before making any investment decisions. Investing can be risky and may not be suitable for all investors. All data sourced from company filings, earnings calls, announcements, and publicly available analyst research as of April 1st, 2026.

Staying convicted. TurboQuant doesn’t kill demand, it creates new use cases. MU still filling only 50-67% of orders. HBM sold out through 2026. LG 🚀

Micron is one of the more analytically interesting semiconductor names right now because it sits at the intersection of two demand cycles with very different timing profiles: the structural AI memory buildout, which is long-duration and supply-constrained, and the consumer DRAM cycle, which is mean-reverting and currently working through a correction. The Monte Carlo simulation approach is appropriate here because MU's earnings are highly sensitive to DRAM and NAND pricing, which are themselves volatile and correlated to global capex cycles rather than company-specific fundamentals. The risk in any valuation that anchors to current HBM demand is that HBM margins are exceptionally high right now because supply is tight relative to the hyperscaler ramp. As Samsung and SK Hynix scale their HBM output through 2026, the pricing dynamic shifts and Micron's differentiated margin advantage compresses. The question the Monte Carlo should stress-test is what happens to the valuation range if HBM pricing normalizes 20 to 30% over the next 6 quarters, because that is the scenario the market seems to be partially pricing in already.