NVIDIA (NVDA) Executive Summary: When Your Best Customers Become Your Worst Rivals

Competition Intensifying: Broadcom's custom AI chips for Google reportedly 40% cheaper to run, AMD ramping up MI308 shipments and Amazon, Google, Microsoft all developing in-house AI chips

Company Overview

NVIDIA is a leading computing infrastructure company, providing advanced graphics, compute, and networking solutions globally. The company operates primarily through two segments: Compute & Networking, which includes data center accelerated computing platforms and AI solutions, and Graphics, offering GPUs for gaming and professional visualization.

NVIDIA is renowned for its innovation in AI, leveraging its foundational CUDA programming model and extensive software stack to address computationally intensive tasks across various industries. Its products are widely used in markets such as gaming, professional visualization, data centers, and automotive.

The company’s data center solutions are critical for AI model training and inference, while its gaming products, including GeForce GPUs, enhance the gaming experience with high-quality graphics.

NVIDIA also supports autonomous and electric vehicle solutions through its automotive platforms.

The company’s strategy involves a platform approach, integrating hardware, software, and services.

Price Action & Technical Context

Price: $170.94 (as of Dec 17, 2025), down from recent highs around $199 in early November:

3-month decline: ~14% off November peak

Currently testing the $170 support level, showing weakness after rejection at $185-$190 zone

Volume: Elevated on down days (220M+ shares), suggesting distribution

NVDA has broken down technically. The stock peaked at ~$207 in late October and has since established a clear downtrend with lower highs and lower lows.

Fundamental Performance

Recent Earnings (Q3 FY2026, Nov 19, 2025):

EPS: $1.30 (beat by 6.56%)

Revenue: $57.0B (beat by 3.9%)

YoY Growth: Revenue +62.49%, EPS +60.49%

The concern: While still exceptional, growth rates are decelerating:

Q1 FY26: Revenue +69%, EPS +57%

Q2 FY26: Revenue +56%, EPS +53%

Q3 FY26: Revenue +62%, EPS +60%

This is down sharply from the 200%+ growth rates seen in early 2024.

Market Sentiment & Positioning

Analyst Coverage: Overwhelmingly bullish

50 recent analyst actions since September, virtually all “Buy” ratings

Price targets recently raised: Morgan Stanley to $250 (Dec 1), Evercore to $352, Loop Capital to $350

This creates crowding risk, everyone already owns it

Relative Strength: Major red flag

Quarterly relative performance vs S&P 500: 46th percentile (as of Dec 16): This means NVDA is now underperforming 54% of S&P 500 stocks

Was in 89th percentile in September, a dramatic reversal: NVDA Relative Strength collapsing from 89th to 46th percentile in 3 months

Insider & Institutional Activity: Warning Signs

CEO Jensen Huang: Systematic daily selling

Selling 25K-75K shares every single trading day since June: Total disposed: $1.5B+. While on a pre-planned schedule, the volume is notable

Institutional 13F Activity (Q3 2025):

Major sellers: FMR (Fidelity) -$2.8B, Nuveen -$1.6B, Capital World -$1.5B, Edgewood -$716M

Major buyers: BlackRock +$3.6B, Capital Research +$4.3B

Net effect: Mixed, but some smart money reducing exposure

Congress Trading: Bipartisan selling in October-November after peak, though some buying on dips

Regulatory & Competitive Headwinds

Export Controls:

Until Dec 15th, China market effectively cut off for H100/H200/Blackwell chips

New “AI Diffusion” rule (Jan 15, 2025) imposes worldwide licensing on advanced chips

Company admits: “Our competitive position has been harmed by existing export controls”

The China Problem:

Company revenue from China declined significantly

CEO Huang stated China could “build a hospital in a weekend”, warning of their infrastructure advantage

Chinese competitors (Huawei, Moore Threads) gaining ground domestically

Competition Intensifying:

Broadcom’s custom AI chips for Google reportedly 40% cheaper to run

AMD ramping up MI308 shipments

Amazon, Google, Microsoft all developing in-house AI chips

Intel reentering with potential $1.6B SambaNova acquisition

News Sentiment: Shifting Narrative

Recent headlines reveal cracks:

Michael Burry warning of “depreciation time bomb” for GPU buyers

Reports of Oracle data center delays

Analysts questioning sustainability of AI spending

Moody’s warning about AI over-investment and debt risks

IBM CEO noting “AI data center economics are at risk”

Valuation Reality Check

Trading at 38.7x forward earnings and 1.02x forward PEG

Growth decelerating from 200%+ to 60%

The market is starting to question whether current valuations are justified if growth continues to slow.

Bottom Line

NVIDIA continues to hold the throne as the undisputed leader of AI infrastructure, but the technical and fundamental cracks are becoming harder to ignore. We are currently witnessing a distinct technical breakdown characterized by a loss of momentum and a shift into a clear downtrend. Perhaps most telling is NVIDIA’s emerging relative weakness; after months of carrying the indices, the stock is now underperforming the broader market. If the current support at $170 fails to hold, investors should prepare for a further slide into the $150–$160 range as the market re-evaluates the stock’s near-term trajectory.

While the company is far from a “bubble” in the traditional sense, it is exhibiting classic late-stage bull market characteristics. We are seeing a confluence of peak valuations and growth deceleration, where results remain strong, but the rate of acceleration is flattening. This is compounded by an increasingly crowded competitive landscape, as major hyperscalers transition from NVIDIA’s best customers to their most formidable competitors by developing in-house silicon. Furthermore, the “universal praise” from Wall Street analysts has become a contrarian red flag, suggesting that bullish sentiment may finally be maxed out.

Looking ahead, the long-term thesis for NVIDIA remains rooted in its dominance of the AI chip sector, yet the “growth premium” that fueled its meteoric rise is under pressure. Broader macro concerns regarding the actual ROI of AI investments are forcing the market to question if we’ve reached a period of over-investment. As the industry matures and regulatory scrutiny intensifies, NVIDIA’s path to further upside will likely be narrower and more volatile than the era of easy gains we’ve seen over the past year.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. All opinions expressed are my personal views. Always do your own research and consult with qualified professionals before making investment decisions.

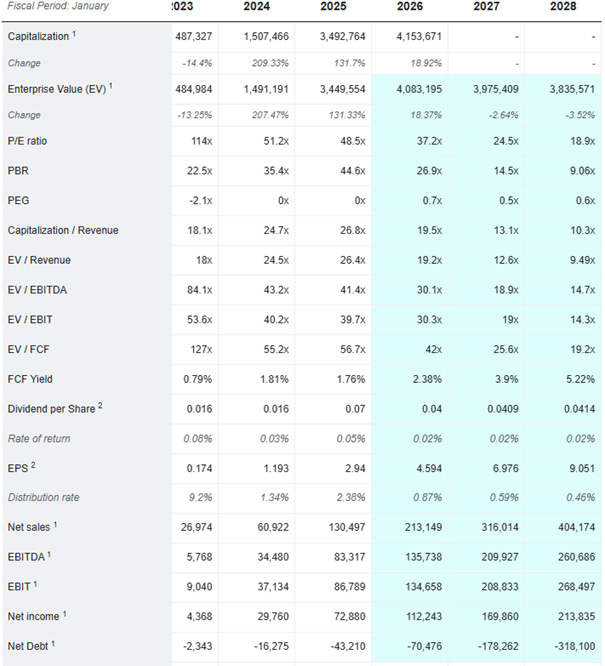

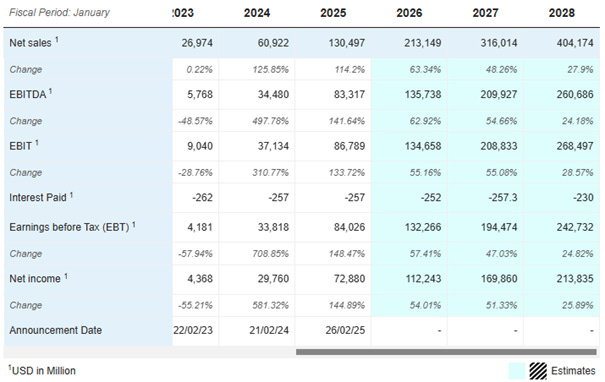

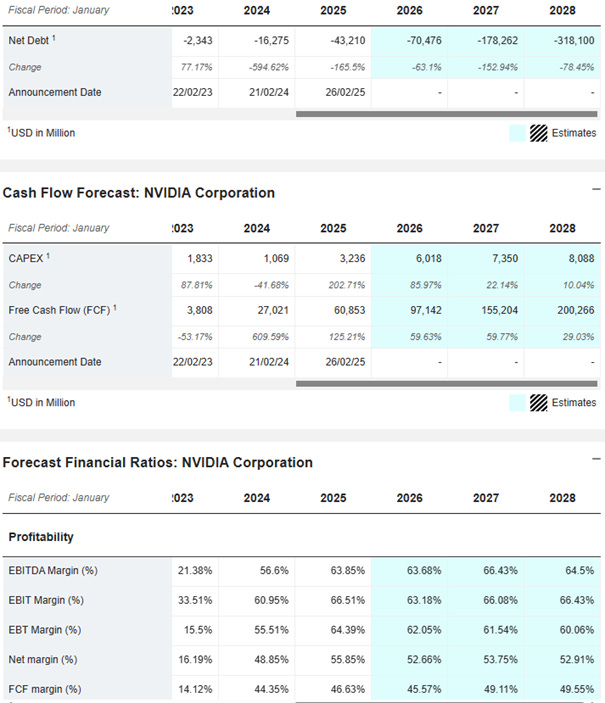

Appendix 1: Financial Projections

Appendix 2: Valuation Metrics