Watchlist Update (June 2026)

Reward / risk, expected value and financial-quality diagnostics. Get the edge you need! Unlock the full story behind these picks by diving into our exclusive articles and deep-dive analyses.

Disclaimer: For informational purposes only, no investment advice.

Every position carries both legs of a bet. The upside leg is the distance from today’s price to estimated fair value; the risk leg is the distance down to the trend stop, the point at which the thesis is wrong on the chart. Dividing the first by the second gives a reward-to-risk ratio. Expected value then weights the two legs by the odds of each, win-probability times upside minus loss-probability times downside-to-stop, which is why our quantitative ranking is sorted by expected value rather than raw upside.

This update folds the long-term fundamental portfolio and the “tactical” list into a single ranking. 50 names. Let’s go.

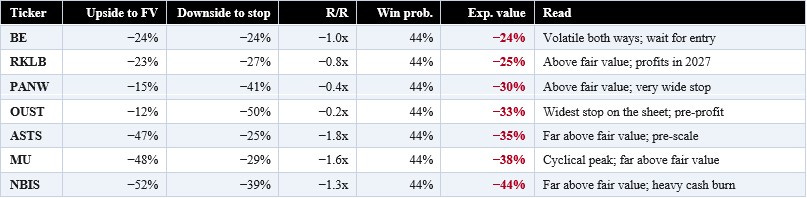

The Quantitative Ranking

Two caveats. The model is binary, it assumes a name either reaches fair value or stops out and ignores the muddle-through middle, so expected value is a ranking signal, not a return forecast. And win probability is a judgment input: the core-book names carry hand-set probabilities, while the tactical names use a consistent rule, a base rate from conviction, adjusted for valuation, with a penalty above fair value. Read the figures as relative, not absolute.

Key Observations

Best stocks are not best buys. The largest winners (CRWD, TSM, NET, GOOG, NVDA from the book) and several quality names that have run to or past fair value (ASML, Eli Lilly, Cadence on the radar) fall to negative expected value, more downside to their stops than upside to their targets.

Tight stops flatter reward-to-risk. Amazon screens at 12.3x and Alibaba at 131x only because their stops sit 2% and 1% below the price, a whipsaw waiting to happen on a long-term compounder, not protection. The ratio is a lens, not a verdict.

The cleanest high-EV names span both lists. MELI, NU, SE and NOW from the book, and Alibaba and Broadcom from the radar, pair high expected value with quality. Others rank high on expected value alone, Hims & Hers and SoFi among them, and the quality overlay separates the two.

Several names trade through their trend stop. Regeneron, Lemonade, Robinhood, Grab and Cameco show a stop above the current price, which inverts the downside leg and overstates expected value; the trend has already broken, so read these as structure-impaired regardless of headroom.

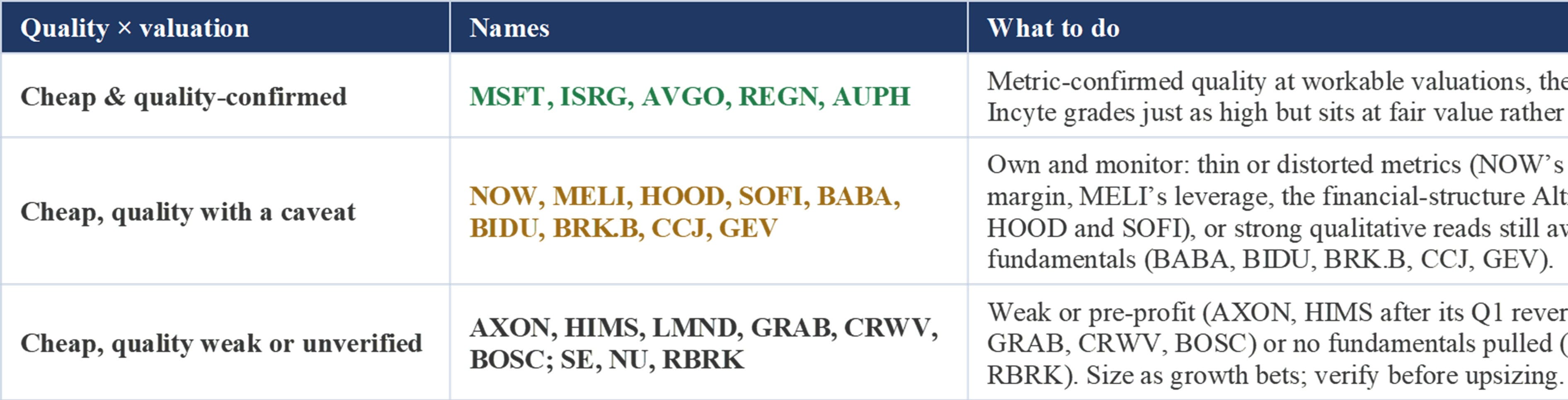

Quality Overlay: Cheap-and-Great vs. Cheap-and-Fragile

Reward and risk graded prices, not businesses. Layering in financial quality supplies the missing axis. The scorecard below grades both cohorts on the same metrics, margins, ROIC, free cash flow, leverage and bankruptcy risk, and is sorted by grade.

What the Quality Lens Shows

It confirms the cleanest ideas across both lists, and surfaces a cheap one. MSFT and ISRG from the book, and Broadcom, Regeneron and Aurinia from the tactical list, pair fortress balance sheets with strong margins. The standout is Incyte, the highest-quality cheap business on the sheet, a 91.8% gross margin, zero debt and a P/E of 14x, held just off the adds list by a thin distance to fair value, not by the business.

It flags where conviction runs ahead of the fundamentals. MELI tops expected value but is now substantially a lender, with leverage swinging to +4.9x and its Altman Z in the grey zone; the debt build is the single thing that would break the thesis. The same financial-institution distortion sits on SoFi and Robinhood, whose Z-scores read as distress when the businesses are not; read their cash-flow trends instead.

It downgrades two names from quality to growth. AXON pairs strong reward and risk with a growth profile, not a quality one, a negative operating margin and persistent negative free cash flow. Hims & Hers reversed sharply in Q1 2026, a negative operating margin and an Altman Z that collapsed from 22 to 3.2. Both belong with the emerging-growth names, sized for the risk that the profitability inflection slips.

Bottom line

Three lenses across one combined universe give a cleaner hierarchy than any list alone. The unambiguous, quality-confirmed buys are MSFT and ISRG from the book and Broadcom, Regeneron and Aurinia from the tactical list; Incyte is the cheapest high-quality name, held back only by valuation. The own-with-a-watch names are NOW and MELI on leverage, plus SoFi and Robinhood on distorted scores. The downgrades, AXON and Hims & Hers, and the pre-profit cohort, move to higher-variance, size-accordingly status. The lesson holds in both directions: high expected value is not a high-quality bet, and high quality is not always a high-EV one, and the cleanest decisions sit where the two line up.

In the V&M Library

MELI (MercadoLibre): The “Amazon of Latin America,” operating a dominant integrated flywheel of e-commerce, the Mercado Pago fintech ecosystem, and a massive logistics network. Deep Dive available here.

AMZN (Amazon): A global leader in diversified retail and cloud computing (AWS) that is currently scaling its own custom AI silicon (Trainium/Graviton) to protect its massive margins. Despite its massive scale, it remains a top long-term pick. Deep Dive available here.

META (Meta Platforms): The world’s largest social media entity, operating Facebook, Instagram, and WhatsApp while pivoting heavily into AI and metaverse hardware. A top long-term pick. Article available here.

MSFT (Microsoft): An enterprise powerhouse that has evolved from a software giant into the backbone of global AI infrastructure through its Azure cloud and OpenAI partnership. Expectations are finally meeting the reality of infrastructure scaling, providing a disciplined entry point for those who believe in the Azure re-acceleration story. Deep Dive available here.

TSM (Taiwan Semiconductor): The world’s largest dedicated semiconductor foundry, serving as the essential “foundry to the world” by manufacturing the advanced 2nm and 3nm chips for Apple and NVIDIA. Deep Dive available here.

Micron (MU): A global leader in memory and storage solutions (DRAM and NAND), currently riding the “AI cycle” due to high demand for HBM (High Bandwidth Memory). High conviction and strength. Though cyclically sensitive, it is currently benefiting from significant AI tailwinds. Both a Deep Dive and Article are available.

Novo Nordisk (NVO): A global leader in diabetes and obesity care, currently transitioning through a “Market Maturity Cycle” as it scales its GLP-1 blockbuster treatments (Ozempic and Wegovy). High conviction and scientific dominance. Despite intensifying competition. Deep Dive available here.

Duolingo (DUOL): The world’s most popular mobile learning platform, currently riding the Personalized Learning Cycle by integrating generative AI into its core curriculum. High conviction and brand strength. By leveraging its massive database of user interactions, Duolingo is evolving from a simple translation tool into a sophisticated AI tutor. Deep Dive available here.

GOOG (Alphabet): The dominant force in global search and digital advertising, now aggressively integrating generative AI across its Google Services and rapidly expanding Cloud ecosystem. Article available here.

AXON (Axon Enterprise): A public safety leader providing a connected ecosystem of TASER devices, body cameras, and AI-driven cloud software for law enforcement. Article available here.

CRWD (CrowdStrike): A cloud-native cybersecurity pioneer using its Falcon platform to provide unified endpoint protection and threat intelligence. A top long-term pick in cybersecurity. Article available here.

RBRK (Rubrik): A data security and cyber-resilience firm that specializes in zero-trust data management and rapid ransomware recovery for enterprises. A high-growth data security firm with 48% revenue growth. Article available here.

ZS (Zscaler): A specialist in cloud security that enables “Zero Trust” architecture by securely connecting users and applications regardless of location. Article available here.

SYNA (Synaptics): A semiconductor firm transitioning from touchpads to advanced Edge AI processors, sensing, and wireless connectivity for IoT devices. An edge computing play with beginner conviction and medium strength. It is expected to turn profitable in 2025/2026. Article available here.

SE (Sea Limited): A Southeast Asian tech giant encompassing Shopee (e-commerce), Garena (gaming), and SeaMoney (digital financial services). Article available here.

JMIA (Jumia): Often called the “Amazon of Africa,” it operates a leading pan-African e-commerce marketplace, logistics service, and payment platform. Article available here.

NVDA (NVIDIA): The primary architect of the AI era, designing the high-performance GPUs and “Vera Rubin” computing platforms that power nearly all modern data centers and AI training. It remains a core AI play but lacks the “Buy Now” trigger. Article available here.

ALAB (Astera Labs): A critical AI-silicon “pure play” that designs high-speed connectivity solutions to remove data bottlenecks within AI server clusters and hyperscale data centers. Article available here.

NU (Nu Holdings): A disruptive digital banking giant (Nubank) that has captured the majority of the Brazilian market by offering low-cost, mobile-first financial services to the unbanked. Article available here.

Eli Lilly (LLY): A pharmaceutical powerhouse dominating the metabolic health space with its blockbuster GLP-1 treatments for diabetes and obesity. It holds Medium conviction but Very High fundamental strength, justifying its demanding valuation. Article available here.

Broadcom (AVGO): A diversified semiconductor and infrastructure software giant that designs custom AI accelerators (TPUs) and high-speed networking chips. A top-tier semiconductor play with High conviction and Very High fundamental strength. It is a cash-flow machine ($8B FCF in Q1 2026) benefiting immensely from custom AI accelerators. Article available here.

ServiceNow (NOW): An enterprise cloud platform that automates digital workflows, now integrating “GenAI” to significantly boost corporate productivity. Despite some sector volatility, it maintains High conviction and High fundamental strength. It is viewed as a contrarian quality play amid AI-driven software disruption fears. Article available here.

ASML (ASML): The world’s only provider of the EUV lithography machines required to “print” the world’s most advanced AI and processor chips. A technological fortress in the semiconductor industry. With Very High long-term conviction and fundamental strength, it remains an irreplaceable. Article available here.

Palo Alto Networks (PANW): A global cybersecurity leader successfully pivoting to a “platformization” strategy to consolidate firewall, cloud, and endpoint security. A cybersecurity titan with High conviction and strength. Its “platformization” strategy is driving strong, consistent cash flow. Article available here.

Intuitive Surgical (ISRG): The global pioneer in robotic-assisted surgery, known for its Da Vinci systems that enable minimally invasive procedures with high precision. It carries High conviction and Very High fundamental strength with solid cash flow generation. Article available here.

Synopsys (SNPS): A critical provider of Electronic Design Automation (EDA) software used by engineers to design and test the world’s most complex microchips. It has Very High conviction and strength, but margins are currently compressing due to integration costs. Strong cash flows despite trading near its fair value. Article available here.

Cadence Design (CDNS): A top-tier competitor in the EDA space, providing the software, hardware, and IP essential for designing advanced semiconductors and electronic systems. Similar to Synopsys, it shows High conviction and Very High strength, delivering excellent numbers in the EDA software space. Article available here.

Teradyne (TER): A leading supplier of automated test equipment used to ensure the functionality of semiconductors, electronic systems, and industrial robotics. An attractive play in automated testing. It has Medium conviction but High fundamental strength and consistent cash flow.

Kinsale Capital (KNSL): A niche “Excess and Surplus” (E&S) insurer that leverages a proprietary tech platform to maintain lower loss ratios than traditional competitors. A high-quality small-cap insurer with Beginner conviction but High fundamental strength and a proven business model.

Nebius (NBIS): An emerging European AI infrastructure company building out large-scale GPU clusters to compete in the global cloud computing market. A high-growth, high-risk AI cloud play. It carries Beginner conviction and Low fundamental strength due to heavy capital requirements. Article available here.

CoreWeave (CRWV): A specialized cloud provider built specifically for large-scale GPU acceleration, serving as a critical infrastructure partner for AI labs. A direct AI cloud infrastructure play with Beginner conviction and Mid strength. It is expected to be cash flow negative for several years but offers massive upside. Article available here.

Rocket Lab (RKLB): A leading end-to-end space company providing reliable small-satellite launch services and developing the “Neutron” medium-lift rocket. An execution-focused space play with Low conviction and Low fundamental strength. Profitability isn’t expected until at least 2027.

One Stop Systems (OSS): A specialist in “ruggedized” high-performance computing (HPC) for the edge, focusing on AI applications in military and industrial robotics. A speculative robotics moonshot. With Beginner conviction and Low strength, it lacks a clear timeframe for profitability.

Lemonade (LMND): A digital-native insurance provider using AI and behavioral economics to automate claims and underwriting for renters, homeowners, and car owners. An AI-driven insurance disruptor. It holds Medium conviction and Medium strength, with high demand but no expected profitability for several years.

Bloom Energy (BE): A green energy firm that manufactures solid oxide fuel cells (SOFC) to provide on-site, reliable “microgrid” power for data centers and hospitals. An energy momentum play with Beginner conviction and Medium strength. It is expected to become profitable moving forward.

Hims & Hers Health (HIMS): A multi-specialty digital health platform that provides personalized, direct-to-consumer access to treatments for hair loss, weight loss, and more. A volatile bet on personalized medicine. It has Beginner conviction and Medium strength, though it is showing volatile but positive margins. Article available here.

Alibaba (BABA): A global e-commerce and cloud powerhouse that dominates the Chinese retail market while aggressively pivoting to proprietary LLMs and AI services. A value-driven play in China with Medium conviction and High fundamental strength. It remains “cheaply valued” relative to its expansion into AI. Analysis available here.

Cameco (CCJ): One of the world’s largest providers of uranium, positioned as a critical fuel supplier for the nuclear plants powering AI-driven electrical grids. A leader in nuclear energy with Beginner conviction and Low fundamental strength. It is riding the wave of high electricity demand for AI.

Celestica (CLS): A high-tech design and manufacturing partner that builds the complex optical networking and storage hardware required by hyperscale data centers. Benefiting from cloud connectivity. It has Beginner conviction and good strength, with margins that are thin but expanding. Fair value: $348. A deep dive (here) and article available here. Investment excited at +27% gain in less than 1 month.

IREN Limited (IREN): A renewable-energy data center operator aiming for $3.4B in AI Cloud ARR by the end of 2026 through massive GPU clusters and secured power. Article.

Applied Digital (APLD): A high-performance computing (HPC) specialist that has successfully transitioned from crypto hosting to elite, large-scale AI infrastructure. Article.

Twilio: (TWLO): A communications giant integrating “”Customer AI”“ to provide predictive engagement, focusing on GAAP profitability in a mature 2026 software market.” Article.

Oracle (ORCL): A cloud powerhouse whose OCI Gen2 has become the primary infrastructure partner for NVIDIA’s sovereign AI and large-scale LLM training. Article.

Applied Materials (AMAT): The fundamental equipment maker for the $1T semiconductor industry, leading in 2026 “”Advanced Packaging”“ and 2nm logic chip fabrication. Article.

Advanced Micro Devices (AMD): The primary GPU challenger to NVIDIA; its MI450 lineup has secured significant 2026 market share among hyperscalers seeking supply diversity. Article.

Lam Research (LRCX): A wafer-fab equipment specialist critical for the production of HBM3E memory and the complex 3D stacking required for 2026-era AI chips. Article.

Ichor Holdings (ICHR): A key supplier of fluid delivery subsystems for chip manufacturing, benefiting from the global 2026 build-out of new facilities in Mexico and Malaysia. Article.

Marvell (MRVL): An infrastructure leader specializing in high-speed data interconnects, solving the critical “”bandwidth bottleneck”“ in massive AI data centers. Article.

Microchip (MCHP): A diversified semiconductor giant providing the “”brains”“ for 2026 industrial automation and smart-edge devices through AI-integrated microcontrollers.” Article.

Intel (INTC): A “”Western Foundry”“ turnaround play betting on its 18A node and disaggregated design to regain leadership in the 2026 PC and server markets. Article.

Core Scientific (CORZ): A massive power-infrastructure player that has pivoted its high-wattage capacity from Bitcoin mining to hosting high-density AI compute. Article.

Palantir (PLTR): The dominant “”AI Operating System”“ for both defense and commercial sectors, successfully scaling its AIP platform into 2026 enterprise workflows. Article.

Tesla (TSLA): An AI and robotics conglomerate focused on the 2026 commercialization of FSD licensing and the deployment of Optimus humanoids in manufacturing. Article.

Lattice Semi (LSCC): The leader in low-power FPGAs, essential for 2026 “”Edge AI”“ applications in robotics, drones, and energy-efficient consumer electronics. Article.

Onto Innovation (ONTO): A high-growth metrology player providing the inspection tools mandatory for high-yield production of complex 2026 chiplet architectures. Article.

VEON (VEON): A global telecom operator in frontier markets aggressively pivoting to “”AI-first”“ digital services (finance/media) to drive ARPU growth in developing economies. Article.

LG Display (LPL): A hardware leader navigating a 2026 turnaround fueled by the “”AI PC”“ cycle and the transition of high-end laptops to tandem OLED technology. Article.

Globant (GLOB): A premier IT consultancy scaling “”AI Pods”“ to help Fortune 500s move from experimental AI pilots to full-scale operational intelligence. Article.

TransMedics (TMDX): A healthcare innovator using AI-optimized logistics and its OCS platform to dominate the “”organs-as-a-service”“ market with 50%+ growth. Article.

Uniti Group (UNIT): A fiber infrastructure REIT acting as the “”physical layer”“ for 2026 AI edge computing by connecting local data centers to the national grid. Article.

Five9 (FIVN): A cloud contact center leader leveraging GenAI to automate CX; by 2026, AI-driven subscriptions account for 50% of its enterprise revenue. Article.

PagSeguro (PAGS): A Brazilian fintech powerhouse utilizing AI for hyper-localized credit scoring and fraud prevention to maintain leadership in the LatAm digital payments war. Article.

AudioEye (AEYE): Provides physical AI sensing solutions for vehicle autonomy, advanced driver-assistance systems (ADAS), robotic vision applications, and non-automotive applications. Article.

Our Investment Approach

Our investment strategy is built on a “Core and Satellite” framework that balances long-term stability with active profit-taking. The “Core” comprises 60-70% of the portfolio, dedicated to a “Buy & Hold” approach for steady compounding. The remaining 40-30% acts as a “Satellite” engine, designed to capture short-term gains by trading volatility during sideways or choppy markets. This dual-layered structure ensures that while the bulk of your capital grows quietly, the active portion works to generate extra returns when the broader market lacks a clear direction.

Selection within this framework is governed by a Value-Momentum filter that combines fundamentals with market timing. First, you identify “Value” stocks trading at a discount to their intrinsic value to ensure a margin of safety. However, to avoid value traps, cheap stocks that continue to fall, you only enter a position once the stock shows “Momentum”, defined as positive price performance over the last 6 to 12 months.

This combined approach ensures you only buy undervalued assets that have already begun their recovery, while simultaneously preventing you from buying hot momentum stocks that have become dangerously overvalued bubbles. We especially look at the second derivative because the market usually “prices in” the first derivative. If a company is already “high quality,” everyone knows it, and the stock is expensive. The biggest gains come from identifying quality compounders transitioning from “average” to “great.” The second derivative is essentially the search for inflection points.

Disclaimer

This report is provided strictly for informational purposes and does not constitute financial advice, an offer to sell, or a solicitation to purchase any securities. The author may hold a position in securities discussed. The analysis reflects independent research conducted without external compensation or existing business relationships with the mentioned entities. Please be advised that investing involves significant risk, and past performance is never a guarantee of future market results. Readers should conduct their own due diligence or consult a licensed professional before making any investment decisions based on this data. All information is sourced from public filings and is considered current only as of June 8, 2026.

Join the Value & Momentum Portfolio

Institutional-grade equity research from a former Lazard and Rothschild & Co investment banker. I’m Denis D., and I bring sell-side rigor to in-depth fundamental coverage paired with high-conviction momentum setups. Each week, my proprietary screens deliver a decisive data edge: Sell-side upgrades, insider and institutional fund flows, aggressive options activity, and second-derivative growth analysis by sector. Subscribe to start your analysis now.

Excellent update! AXON is not an easy business to study, if you look at them at the surface level with their financial statements and margin trends, they don’t appear to be a high quality company.